Miami Condo Investments’ Most Popular Buildings in Greater Downtown Miami

I thought about doing a TBT post today, but then changed my mind. There is so much going on in today’s real estate market, why talk about the past? New buildings are opening every month, people are curious about how these new buildings compare to the ones that were new in years past. So which buildings are currently the most popular by condo shoppers?

I took a look through our Google Analytics report to see what our readers are looking at the most. In the time period from May 14, 2017-June 14, 2017, MiamiCondoInvestments.com received a total of nearly 73,000 page views. Of those, here are the ten most viewed building pages. This list does not include views of individual listings, just of the building pages themselves, where you can find inventory lists, market statistics and closed sale/rental data.

1 – SLS Brickell – 1,219 views

It makes sense that SLS Brickell would take the number one spot with an overwhelming lead. The project was very much anticipated by future tenants, owners and pool-party-goers alike. Move-ins began in late December/early January and have moved on at a rapid pace, leaving the building almost at full occupancy now, with demand still strong. Our agents alone have handed out 16 sets of keys in the building, with a healthy book of buyers and prospective tenants still shopping.

2 – Reach at Brickell City Centre – 731 views

I would have been surprised if Brickell City Centre didn’t make this list! This project was the catalyst that fueled the buying craze in Brickell over recent years and reinvigorates the neighborhood that was once a dense yet sleepy enclave of beautiful high rises that became quiet at night. Reach was the first residential tower to open in Brickell City Centre, and is also approaching occupancy. When the project initially opened, one bedrooms started at $2,400-$2,450/month, but now have risen to $2,650/month.

3 – Brickell Heights East – 715 views

The newest new building on the block also made the list, and no surprise there. Our photo tour of Brickell Heights just days before they opened was one of the most popular blog posts so far this year, and the amount of calls we get for it is a very good sign that the initial occupancy of the building will go smoothly.

4 – 1100 Millecento – 700 views

Millecento’s place as number 4 on the list was a bit more surprising, but not in a bad way. It’s not the newest building in the area, so people aren’t hungry for a preview. There’s really no drama going on with the building (that I have heard of at this time), so people aren’t looking for gossip and info. We still receive a healthy amount of calls and contact requests on Millecento, so I feel it’s safe to say that the traffic is good ol’ prospective residents. That’s great!

5 – Biscayne Beach – 638 views

Edgewater’s newest new building is also on the charts. We covered the progress & opening extensively, so it makes sense that blog readers are interested in the progress. We also have a beautiful 3 bedroom unit listed on the 30th floor with direct bay and Downtown Miami views. It is well-priced and a blank canvas inside. With the amount of attention the building receives, I feel that it will sell quickly.

6 – The Bond on Brickell – 615 views

The Bond is very popular for people who want to live in a brand-new condo in Brickell, but prefer understated elegance and high quality finishes over the kitschy excess that is SLS Brickell. We receive many calls about this building, and there have also been many of our clients who have called about SLS Brickell but then chosen The Bond. It is like SLS Brickell’s quieter sister.

7 – The Plaza at Brickell East Tower – 531 views

The Plaza is basically a Brickell staple. I was surprised that it received more views than any of the IconBrickell towers, but that just shows what the market is interested in. We did a market report on Monday about The Plaza and found that sellers and landlords fare better in today’s market by removing that horrible outdated berber carpet from 2008. There is too much competition in the neighborhood to expect buyers and tenants to sign up for old berber carpet (in case I didn’t make my point on Monday).

8 – BrickellHouse – 530 views

Despite their garage saga, BrickellHouse remains a popular building in the neighborhood. Yes, the garage is broken. No, we don’t know when it will be fixed. Despite that, the finishes are quite lovely, the views and location are great and it remains very popular among our clients.

9 – IconBrickell Tower 1 – 477 views

Of course IconBrickell would be on the list. It has remained one of our most requested buildings since it opened… even since the pool closed. The pool should reopen by the end of the year.

10 – Jade Residences at Brickell Bay – 468 views

Jade is one of the most luxurious buildings in the neighborhood, even after 13 years. Although most buildings in Brickell have beautiful bay views, Jade is where you go if you want an extremely luxurious setting with private elevators and direct bayfront. The only building it competes with is the Santa Maria, except that Jade is more modern and in a more walkable section of the neighborhood.

Do you think that the top viewed buildings on our website are surprising, or expected?

Market Stat Monday: The Plaza on Brickell

Happy Monday! We’re back! After a two week hiatus for Memorial Day and the opening of Brickell Heights, we are resuming #MarketStatMonday with one of Related Group’s top projects from the last building cycle (2004-2008), The Plaza on Brickell. Typically, when I run a market statistics report for a project with more than one tower, I would separate them into two reports. Since The Plaza on Brickell East and The Plaza on Brickell West are largely similar, I’m going to combine them into one overall project report today.

Between the two towers, The Plaza on Brickell has 1,000 apartments that share a common amenity space above the parking garage. It is pet-friendly and family-friendly. While it is not as trendy or flashy as many other buildings in the area, it is very well-kept, has all of the amenities people ask for in the area, the layouts are nice and it remains a popular choice for our clients.

One thing that we have to watch for at Plaza is that the majority of the apartments were delivered with carpet and the majority of original buyers were investors. At this point, most people have changed the carpet, but we still see the occasional listing pop up with the original 9 year old berber rug that nobody wants. Even though it’s an easy fix, we can see a direct effect in the transaction value on those listings, both for rentals and for sales.

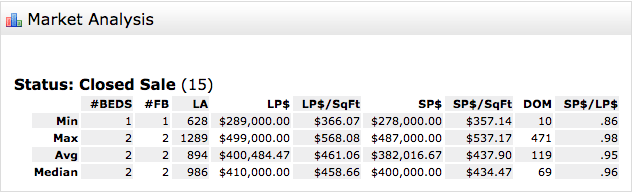

Sales Market

So far in 2017, there have been 15 closed sales that were unfurnished non-penthouse apartments. For those who are new to Market Stat Monday, I leave out the “outliers” on our market report. That would be penthouses, town homes, or apartments that have been combined. Buyers are paying on average $438/square foot for their Plaza condos and sellers are negotiating to 95% of their asking price.

One bedrooms sold for between $278,000-$357,000 and two bedrooms sold for between $400,000-$487,000. Yes, the least expensive units sold with carpet. The lowest priced sale of an apartment with hard flooring (tile, wood, laminate) sold for $320,000…. so there you go.

Looking at what is available, there are 83 active listings of non-penthouse/non-townhouse/non-combined units. The average listing price is $497/square foot. Given the fact that sellers are negotiating on average 95% of their asking price, it looks like eager sellers need to amend their price in order to see results.

The part that I once saw as alarming but now come to expect is that at the current rate of sales, we have 33 months’ of inventory waiting to be sold at Plaza. They don’t have any internal drama or litigation that I have heard of. Their HOA dues are lower than the competing buildings in the area, and the design isn’t so trendy that it alienates a portion of the market… quite the contrary. That brings us back to price. If people want to sell, there is a tremendous competition right now for buyers. The apartments need to be shined up, professionally photographed in their Sunday best, and priced properly. No more 9 year old carpet. That doesn’t fly in this market.

As of today, one bedrooms start at $285,000 for a unit with a Brickell Avenue view and original carpet. We are offering a one bedroom with wood laminate floors and a view of the meditation area near the pool for $330,000. If you’re looking for a two bedroom plan, options start at $399,000 for a carpeted unit with a view of Brickell.

I also saw a two bedroom plan with carpeted floors and a South partial-bay view that was listed for $389,452. It was The Plaza East 950 Brickell Bay Drive #2507. Just when I was writing about what a great deal that was for a buyer, the status changed to pending. Congratulations to that buyer!

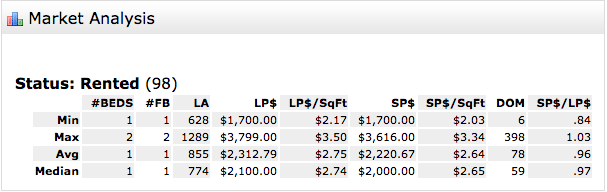

Rental Market

As we have seen in other buildings during recent weeks, the rental market is much healthier than the sales market. With 30 active unfurnished listings and 99 closed rentals this year, we have almost 2 months’ of inventory in the market right now.

Although the rental market is healthier, the marketing time is on average 78 days, including the time a prospective tenant undergoes their background checks. The apartments that found tenants accepted 96% of their asking price, so again… this is not a fire sale opportunity for tenants who are interested in over-negotiating.

Just like in the sales market, we are seeing the lowest priced listings still have that original 2008 berber carpet that has seen as many as 10 tenants. Even with shampoo, nine year old carpet is beyond its’ intended life span and should be changed. One bedrooms rented between $1,700-$2,200 per month and two bedrooms garner between $2,400-$3,616 per month, with the more expensive rentals being larger plans with hard floors and superior views.

My biggest takeaway for today’s look into The Plaza is that if you are looking to increase your return, whether it be on the rental or the sales market, the first thing you should do is CHANGE THE CARPET! What is your biggest takeaway from The Plaza?

Just Listed – 2 Bedroom Corner Unit at The Plaza on Brickell with Direct Water Views – Asking $825,000

I am pleased to announce my newest listing – unit 3211 at The Plaza on Brickell – a 2 bedroom, 2.5 bath corner unit with breathtaking views of Biscayne Bay, Brickell Key, and Key Biscayne. This is an 11 line unit located on the 32nd floor of the Brickell Bay tower, arguably the best line in the entire development. Most importantly, the unit clears the Four Ambassadors across the street by 12 floors, allowing for direct water views. As one would expect, units that clear the Four Ambassadors sell at a big premium to those that do no. Last September, unit 3411 – just two floors directly above unit 3211 – sold for $850,000. That unit was sold furnished with marble flooring throughout. Priced to sell, unit 3211 is being offered for $825,000.

The Plaza on Brickell is centrally located, just blocks from the shops, restaurants, and bars at Mary Brickell Village and the upcoming $1.2B mixed-use development called Brickell City Centre. Amenities at The Plaza on Brickell include: two swimming pools, hot tub, steam room, two fitness centers, 24-hour concierge, 24-hour valet parking, club room, theater, and more.

Brickell Condo Tour and Construction Update [VIDEO] – February 14, 2015

It has been about four months since my last video tour covering the fast-paced development taking place in Brickell. Since then, a lot has happened, so I figured it was time to get back out on the road and provide everyone with another update. As you will see, this video is much more comprehensive, covering not only current and future construction, but also existing condo developments for those who may be unfamiliar or newly acquainted with the Brickell condo market. In the video, I even highlighted two, large commercial properties in Brickell which recently traded hands – the SunTrust building located at 777 Brickell Avenue, which sold earlier this week for $140M, and the former Capital at Brickell site located at 1420 South Miami Avenue, which was acquired this past December for $74.74M by CCCC International USA LLC, a subsidiary of Beijing’s China City Construction and American Da Tang Group of New York.

The rental market is a very interesting segment of the real estate market, not only for potential tenants on the prowl for a new pad but also current landlords and would-be investors trying to assess the demand for rentals across various neighborhoods and, more specifically, across various condo developments. Only a few years ago, the supply of rentals in Miami far outpaced demand. As a result, rental prices plunged and renters ruled the day. Fast forward to the present and an entirely different rental market is upon us in Miami. Nowadays, rental inventory is being absorbed quickly and overall rental prices are on the rise. For those living in Miami, I’m sure this a message that you have not only read in the local paper but have also heard directly from friends and family who have experienced it firsthand.

Obviously, not all neighborhoods and condo developments are created equal. Factors such as price, location, views, quality and recommendations from peers help determine rental demand. As a result, one would assume that demand can vary greatly from building to building and even neighborhood to neighborhood. Which condo developments are the leaders when it comes to rental demand and which are the laggards? More importantly, which buildings should we expect to see prices climb in the near future?

In this first segment, I decided to analyze the Brickell rental market to answer the above questions. Below, you will find a spreadsheet containing rental data for various condo developments in Brickell. Click the link below the spreadsheet to view it in its entirety.

Brickell Rental Market as of March 01, 2011

Columns C through G show the number of available rentals pertaining to each condo development grouped by number of bedrooms. Column I displays the total number of rentals available in each condo development while column J shows the total number of units within that development. I debated whether or not to include column K, the number of available rentals over the total number of units in the development expressed as a percentage, because the figure can be deceiving in buildings where developer inventory remains which has neither been sold nor rented. This is the case in buildings such as Icon Brickell and Infinity at Brickell. Regardless, I decided to include the figure because it can provide additional insight in buildings where this is not the case.

The main objective in creating this spreadsheet was to calculate months of inventory for each condo development. This can be seen in column M. Months of inventory was calculated by dividing total units available for rent by the monthly average number of units rented over a 3-month period from November 16, 2010 to February 15, 2011. You may be wondering why I did not include closed rental data from the past two weeks in determining the monthly average. I have noticed that it can take real estate agents days, and even weeks, to change the status of a rental in the MLS from pending to rented. As a result, I felt that the average would be skewed to the downside and not be an accurate representation of the Brickell rental market. Furthermore, if I had to venture a guess, I would also say that it is highly likely that around 10 percent of the total number of units available for rent are in fact no longer available. In this case, the listing agent has yet to change the status from available to pending.

Regardless, a lot can be ascertained from the spreadsheet above. In my opinion, any building with 1.5 months of inventory or less has a solid rental market. 1060 Brickell, The Plaza on Brickell and Vue at Brickell are standouts with absorption rates hovering around one month. I expect rentals prices in these developments to continue to rise in the near future. For those in the market to lease a condo in one of these developments, I advise that you act quickly and put your best foot forward when making an offer.

According to the spreadsheet, there is currently 2.29 months of rental inventory available in Brickell. Some may expect this number to increase as more units from Icon Brickell and Infinity at Brickell hit the rental market. Of course, this will all depend on how quickly the units become available and at what pace demand absorbs them. Only time will tell, but I plan to watch Brickell rental market closely and post updates on a monthly basis.

I would love to hear your thoughts and comments.

Brickell Condo Index – August 2010

The Brickell Condo Index is back! It has been a year and a half since I last published the Brickell Condo Index. Fortunately, eighteen months is a good reference point and definitely enough time where one would expect a lot to have changed with the condo market. For those of you who haven’t followed this blog that long, the Brickell Condo Index is an in-depth look at the various condo buildings in Brickell with various statistics included to illustrate the health or weakness of each building.

I hate to be the bearer of bad news but this will be the last Brickell Condo Index to appear on this blog. From here on out, the Brickell Condo Index, as well as other neighborhood indexes, will only be made available via email. Early next week, I will unveil a new version of the Miami Condo Investments website. The new website will be much easier to navigate, have a lot more content, load considerably faster and, most importantly, allow you to register to our Miami Condo Investments weekly newsletter. The weekly newsletter will contain the best condo deals of the week, relevant news stories and exclusive market data such as the neighborhood condo indexes. The neighborhood condo indexes will be emailed the Sunday following the 15th of each month, the day that I have chosen to collect and compile the data. Each neighborhood will be represented every six months as follows: Brickell this month, Brickell Key next month, Downtown Miami in October, the Edgewater in November, South Beach in December and the Miami River area in January. The cycle will then start all over so a neighborhood update is provided twice per year. In the meantime, if you’d like to be included on the newsletter list then simply send us an email at [email protected] and convey your interest to be placed on the list. The blog will not change and will continue to be updated but the market data reports will only be made available via our newsletter.

Before we get into this month’s numbers, let me discuss a few changes that I made to the Brickell Condo Index since the last update in February 2009. First, I excluded One Miami from the index. One Miami will be included in the Downtown Miami Condo Index in October. Second, Latitude on the River and Neo Vertika were also excluded. Both will appear in the Miami River Condo Index in January 2010. Third, I decided to include 1060 Brickell, 500 Brickell, Brickell on the River South and The Plaza on Brickell. Each has had enough closed resales to warrant their inclusion in the Brickell Condo Index. Fourth, I decided to bring back The Sail on Brickell. As of late, I’ve seen much more interest in the building due to its price point and it is much healthier than it was in October 2007 when I dropped it from the index. I guess you can say that it’s officially off the pink sheets. There are now a total of twenty buildings in the Brickell Condo Index whereas before there were eighteen. Last, but not least, I decided to round the price per square foot calculations. I think it makes everything easier to read and I honestly don’t think excluding the two decimal points makes the figures any less insightful.

As per the MLS, the average of the asking prices of the twenty condo buildings that now represent the Brickell Condo Index is $376 per square foot. The average asking price per square foot for each Brickell condo building individually can be found below:

1060 Brickell – 1050 & 1060 Brickell Ave – $375

500 Brickell – 500 Brickell Ave & 55 SE 6 St – $362

Atlantis on Brickell – 2025 Brickell Ave – $255

Brickell on the River North – 31 SE 5 St – $268

Brickell on the River South – 41 SE 5 St – $276

Bristol Tower – 2127 Brickell Ave – $471

Emerald at Brickell – 218 SE 14 St – $348

Four Seasons Residences – 1425 Brickell Ave – $954

Imperial at Brickell – 1627 Brickell Ave – $285

Jade Brickell – 1331 Brickell Bay Dr – $532

Santa Maria – 1643 Brickell Ave – $691

Skyline on Brickell – 2101 Brickell Ave – $352

Solaris at Brickell – 186 SE 12 Ter – $189

The Club at Brickell Bay – 1200 Brickell Bay Dr – $285

The Mark on Brickell – 1155 Brickell Bay Dr – $313

The Palace – 1541 Brickell Ave – $298

The Plaza on Brickell – 951 Brickell Ave & 950 Brickell Bay Dr – $394

The Sail on Brickell – 170 SE 14 St – $299

Villa Regina – 1581 Brickell Ave – $350

Vue at Brickell – 1250 S Miami Ave – $214

At the bottom of this post, I included a chart that shows how each of the above figures compares with those published in February 2009. Solaris at Brickell experienced the largest drop with average asking prices there falling slightly over 40 percent. Three of the buildings saw a slight increase in their average asking price per square foot within the past eighteen months. These were Bristol Tower, Four Seasons Residences and Villa Regina.

Below, you’ll find the average price per square foot for Brickell condos sold in the MLS within the six month period from February 1, 2010 to July 31, 2010. I decided to do it this way because I’ve noted that oftentimes it takes agents a few weeks to change the status of a listing in the MLS from pending to closed. The neighborhood as a whole sold at an average price per square foot of $285 during that time period.

The biggest surprise in the figures above when compared to those in February 2009 is Jade Brickell. The average price per square foot for closed sales during the previous six months increased a little over 14 percent when compared to the figures published eighteen months ago. Other buildings that experienced an increase are Skyline on Brickell, The Mark on Brickell, Villa Regina and Vue at Brickell. With the exception of Villa Regina, these buildings were some of the hardest hit in Brickell when the market collapsed mainly due to the large amount of mortgage fraud that took place in these buildings. The Club at Brickell Bay and Solaris at Brickell are two other buildings in Brickell that were heavily victimized by mortgage fraud. The Club at Brickell Bay saw about a 1 percent decrease in average closed sales prices while prices at Solaris at Brickell fell slightly over 9 percent. This actually makes sense since the fallout at Solaris at Brickell didn’t take place until about a year after the others. Also worth mentioning, prices at Santa Maria fell a little over 4 percent within the past eighteen months but the numbers were a bit skewed due to Penthouse 4901 recently selling for $1,100 per square foot. The average for the past six months would have been much lower had it not been for that sale.

Below you will find some additional statistics. Click on the image to enlarge it.

The first column to the right of each condo development name is the difference in the average sales price and list price for this month, expressed as a percentage. A high percentage indicates that there is a large discrepancy between the average asking price for condos currently on the market and what has actually sold within the past six months. In other words, many of the sellers in these buildings are delusional and are in need of a reality check. For example, 1060 Brickell has a very large discrepancy because there are quite a few units asking over $400 per square foot and even some asking over $560 per square foot while closed sales have averaged around $208 per square foot within the past six months.

The second column shows the number of active listings currently in the MLS for each condo development. The third column shows the percentage that these listings represent over the total number of condo units in each development. The cells highlighted in green reveal those condo developments that have active listings that that represent less than 10 percent of the overall units in the building. This is typically one indication of a sound condo building. When I first started doing the Brickell Condo Index in 2007 many of the cells in this column were highlighted in red, indicating that active listings represented over 20 percent of the building. This was always a good indication that prices would fall further in these buildings. For example, in February 2009, active listings at Solaris at Brickell represented slightly over 20 percent of the building. That was the largest percentage of listings at that time and it is not a coincidence that eighteen months later prices fell the most at Solaris at Brickell of all the buildings represented in the Brickell Condo Index.

The fourth column reveals the number of condos currently pending sale in each building. The Club at Brickell Bay has a whopping 42 pending sales at this time and there are a total of 155 pending sales in all of the buildings combined. In February 2009, there were only 81 pending sales although a total of twenty buildings are now present in the Brickell Condo Index rather than eighteen. The fifth column displays the number of closed sales from February 1, 2010 to July 31, 2010. Once again, The Club at Brickell Bay leads the way with a total of 38 closed sales in that time period. It’s interesting to note that there were 20 more closed sales in the six months prior to February 2009 when compared to the current closing numbers even though the index now has two additional buildings.

The sixth column shows the difference in the average list prices from this month’s and February 2009’s, expressed as a percentage. Those highlighted in red reveal those condo developments which had a drop in their average list price while those highlighted in green show those that experienced an increase.

The seventh column reveals the difference in average sales prices from this month’s and February 2009’s, expressed a percentage. Once again, those highlighted in green represent an increase while those highlighted in red represent a decrease.

Well, that’s all for today. Have fun with the numbers. Time for me to get back to work on the new website.

Shrinking Rental Inventory in Brickell and Downtown

In this episode, we discuss the shrinking rental inventory of condos in Brickell and Downtown Miami. In recent months, it has become increasingly more difficult to find a rental in these neighborhoods than it has since the peak of the market. For example, at this time The Plaza on Brickell, which has 1,000 total units, only has two unfurnished one bedrooms available while 1060 Brickell has zero. We highlight eight other well known condo buildings in these areas and provide an overview of the rental availability within them.

Miami Real Estate Review – Episode 7

In this episode, we provide an update regarding the developer blowout sale at The Plaza on Brickell that started last Thursday. We also touch upon pricing at Icon Brickell and discuss news regarding Marquis. We end the show by highlighting four noteworthy foreclosures that came onto the market since last Friday.

Developer Blowout at The Plaza on Brickell

In this video segment, we discuss the developer blowout sale at The Plaza on Brickell that was announced Thursday afternoon. I received word just 24 hours later that 16 units had already been placed under contract. This is now the best deal in Brickell but availability won’t last long. Later in the video, we also discuss the uptick in luxury condo sales in 2010. We end the show with a picture slideshow of Penthouse A at Apogee South Beach which came onto the market last month with an asking price of $16M.