Closings Begin at The Standard Residences Midtown Miami

First Residential Tower Completed in Midtown Miami in Nearly a Decade

A major milestone has been reached in Miami’s urban residential landscape as The Standard Residences, Midtown Miami has officially been completed and has begun closings. Developed by Rosso Development in partnership with Hyatt and Midtown Development, the 12-story building has secured its temporary certificate of occupancy (TCO), marking the first residential tower delivered in Midtown Miami in nearly ten years.

Located at 3100 NE 1st Avenue, the nearly sold-out development introduces a new pied-à-terre–style residential concept in one of Miami’s most walkable and vibrant neighborhoods, positioned between the Miami Design District and Wynwood.

A Global First for The Standard Brand

The project represents a significant evolution for The Standard, marking its first-ever standalone residential building worldwide. Known for its playful, culture-driven hospitality experiences, the brand brings that same DNA into a full-time residential environment.

“Our vision was to bring The Standard brand’s incredible energy into the fabric of Miami urban living, creating a space with soul that is deeply connected to the community,” said Carlos Rosso, Founder of Rosso Development. “We are excited to welcome our newest residents home to experience the lifestyle and engage with the vibrant social spaces we have created. Midtown is now one of South Florida’s most compelling neighborhoods, and The Standard Residences, Midtown Miami is proud to stand at the center of that transformation.”

This concept blends lifestyle hospitality with everyday living, offering residents not just a home—but an immersive social experience.

Arquitectonica Design with Over 34,000 Square Feet of Amenities

Designed by Arquitectonica with interiors by Urban Robot alongside The Standard’s in-house team, the building delivers a highly curated aesthetic that blends modern architecture with warm, social interiors.

The development includes 228 residences and more than 34,000 square feet of amenity space, reflecting a strong focus on lifestyle and community-driven programming.

Rooftop Pool, Restaurant, and Social Spaces Define the Experience

One of the standout features is the landscaped rooftop, anchored by a 60-foot-long resort-style pool and Solana, a signature rooftop restaurant and bar by the Juvia Group.

The rooftop is designed as a social hub, offering panoramic views and a vibrant atmosphere that aligns with The Standard’s signature lifestyle.

Wellness, Work, and Play: Amenities Built for Modern Living

Residents have access to a wide array of amenities tailored for wellness, productivity, and entertainment, including:

State-of-the-art fitness center

Yoga and stretch studios

Infrared sauna

Co-working and social lounges

Cultural programming and events

Karaoke rooms

Pickleball court that transforms into a disco room

The property also integrates curated food and beverage offerings such as Mannarino, Sushi Garage, Rosetta Bakery Café, and Privato Speakeasy, reinforcing its lifestyle-driven concept.

Prime Midtown Location at the Center of Miami’s Creative Scene

Midtown Miami continues to evolve as one of the city’s most desirable neighborhoods, offering a rare combination of walkability, dining, shopping, and proximity to cultural hubs.

As Amar Lalvani, President and Creative Director of Hyatt’s Lifestyle Group, noted:

“The Standard brand has always gravitated toward neighborhoods with creative energy, places where you can feel life happening on the street. Midtown has that. It’s walkable, it’s connected and it sits right between some of Miami’s most interesting districts. At The Standard Residences, our owners get to fully inhabit The Standard brand, create everyday routines and join a community that will help shape the future of Midtown.”

Nearly Sold Out with Limited Residences Remaining

The completion of The Standard Residences marks a defining moment for Midtown Miami, introducing a new category of branded residential living that merges hospitality, design, and community into one cohesive experience.

For buyers seeking a lifestyle-driven residence in one of Miami’s most dynamic neighborhoods, this project sets a new benchmark—and signals continued growth for Midtown as a premier urban destination.

With closings now underway, The Standard Residences, Midtown Miami is nearly sold out, with only a limited number of residences remaining. Contact us for details at [email protected].

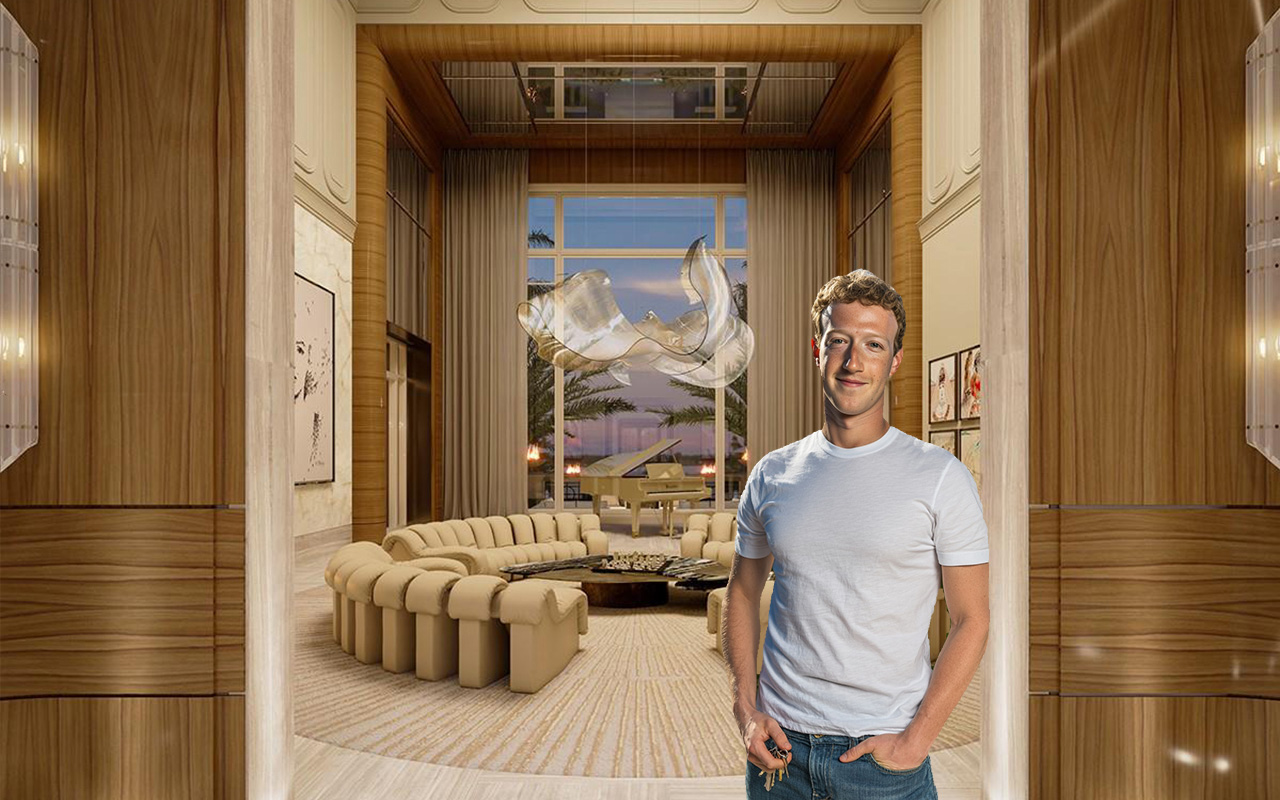

Mark Zuckerberg Drops $170M on Miami Waterfront Mansion

In one of the most high-profile residential real estate deals in South Florida history, Meta CEO Mark Zuckerberg and his wife Priscilla Chan have officially closed on an under-construction waterfront estate on Indian Creek Island for $170 million — marking a record-setting sale in Miami-Dade County and one of the most expensive home purchases in the U.S. this year.

️ What Makes This Purchase Historic

The newly acquired property, located at 7 Indian Creek, sits on approximately 1.84 acres on the ultra-exclusive Indian Creek Island — often nicknamed the “Billionaire Bunker” due to its elite roster of residents and stringent privacy.

Originally listed for $200 million in late 2025 by brokers Danny and Jill Hertzberg of Coldwell Banker Realty, the estate ultimately sold for $170 million, making it the most expensive residential sale on record for the county.

With 9 bedrooms, 11 bathrooms, 4 half bathrooms, and sprawling grounds designed for privacy and luxury, the estate was commissioned by a prominent developer who acquired the land years ago and teamed up with world-class designers to craft a spectacular waterfront compound. Renderings shared earlier this year showed the home’s grand architectural vision — including water views, a private dock, pool, and bespoke interior spaces — all epitomizing the pinnacle of coastal luxury living.

Indian Creek Island: Privacy and Prestige Redefined

Indian Creek Island is one of America’s most exclusive residential enclaves, home to a tiny population of ultra-high-net-worth individuals and families. With its own police force, gated bridge access, and just 41 residential lots, the community offers a level of security and seclusion unmatched by most other luxury markets.

Other notable residents include billionaire tech leaders, entertainment icons, and global financial figures — making Zuckerberg and Chan’s arrival part of an elite neighborhood narrative.

Why This Matters: Market Trends and Billionaire Migration

Zuckerberg’s Miami acquisition reflects a broader trend of affluent buyers expanding their real estate holdings into Florida, particularly as some wealthy individuals consider shifting residency away from high-tax states. The Sunshine State’s lack of a personal income tax, world-class lifestyle, and strong global appeal continue to fuel demand for trophy properties.

While this $170 million sale doesn’t eclipse the highest-ever U.S. residential price (a New York penthouse sold for $238 million), it sets a new benchmark for Miami-Dade County and underscores South Florida’s rising stature on the global luxury real estate stage.

Why Buyers Are Choosing Miami

Experts say several key factors make Miami and Indian Creek particularly appealing to ultra-wealthy buyers:

Unmatched privacy and security in enclaves like Indian Creek.

No state income tax — a significant financial benefit compared with high-tax states.

A global lifestyle hub, blending cosmopolitan culture with waterfront living.

As Miami continues to attract top buyers from around the world, Zuckerberg and Chan’s purchase at 7 Indian Creek solidifies the city’s reputation as a premier destination for the world’s wealthiest homeowners.

Brickell Flatiron Tri-Level Penthouse Fetches $9.212M After 28-Day Auction

Photo Credit: Lux Media Group and Carol Villela

A tri-level trophy penthouse crowning Brickell Flatiron is now pending sale for $9.212 million, closing just 28 days after launching via Sotheby’s Concierge Auctions.

The sale culminated live at ModaMiami at The Biltmore Hotel Miami – Coral Gables, in partnership with RM Sotheby’s and in cooperation with Jonathan Garcia and Elena C. Bluntzer of ONE Sotheby’s International Realty.

The result speaks volumes about the continued velocity at the top of Miami’s luxury condo market when product and platform align.

From $14.9M Listing to $9.212M Pending Sale

Originally listed at $14.9 million and on the market for 285 days, the sellers pivoted to a time-certain auction strategy.

Within 28 days, the property was under contract at $9.212 million.

That compression of timeline highlights how competitive auction environments can drive decisive outcomes for high-end properties that may otherwise linger in traditional listing channels.

As Chad Roffers, CEO and Co-Founder of Sotheby’s Concierge Auctions, stated:

“The successful sale of this penthouse underscores continued demand for design-forward residences in Miami’s premier urban core. Presenting the property during ModaMiami positioned it directly in front of a concentrated audience of luxury collectors and decision-makers, creating competitive momentum that led to a standout result.”

A Designer-Ready Trophy Penthouse in the Sky

Spanning three private floors, the corner penthouse represents one of the most architecturally dramatic residences at Brickell Flatiron.

Key features include:

Over 7,800 interior square feet

Approximately 2,700 square feet of terraces

Five bedrooms

Seven full bathrooms

Two powder rooms

Triple-height ceilings

Dedicated in-residence elevator

Floor-to-ceiling glass captures sweeping 200-degree views of the Miami skyline and Biscayne Bay.

The crown jewel remains the ultra-private rooftop terrace, complete with a private pool, wet bar, outdoor shower, and expansive entertaining space designed for sunrise-to-sunset vistas and moonlit gatherings above the Brickell skyline.

Photo Credit: Lux Media Group and Carol Villela

The Power of the Auction Platform

The sale culminated live at ModaMiami — the premier luxury car collector and lifestyle event — in partnership with RM Sotheby’s. That positioning placed the property directly in front of a highly concentrated audience of luxury buyers and collectors.

Jonathan Garcia noted:

“From its scale and private rooftop pool to its commanding skyline views, this penthouse presented a rare opportunity to own within one of Miami’s most iconic towers. Collaborating with Sotheby’s Concierge Auctions ensured this trophy residence was presented to the right global audience, ultimately finding the ideal buyer.”

The takeaway: in today’s Miami luxury market, strategic exposure matters as much as product quality.

What This Means for the Brickell Luxury Market

The $9.212M pending sale reinforces several important trends:

Continued demand for large-scale, design-forward residences

Strong buyer appetite at the top of the market when pricing aligns

Auction strategies gaining traction for ultra-luxury properties

Brickell’s positioning as Miami’s premier urban core

Completed in 2019, Brickell Flatiron remains one of the most recognizable residential towers in the neighborhood, rising 64 stories with 523 residences in the heart of Brickell — steps from Brickell City Centre, Mary Brickell Village, and directly above Sexy Fish.

Vista Harbor Residences & Yacht Club Launches Sales on the Miami River

Sales have officially launched for Vista Harbor Residences & Yacht Club, a new 12-story riverfront condominium development bringing 242 modern residences and a private marina lifestyle to the heart of Miami. Developed by ALTA Development LLC and designed by FormGroup Architects, the project continues Henry Pino’s vision of transforming the Miami River into one of the city’s most dynamic waterfront corridors.

With 650 feet of direct river frontage, two residential towers with independent lobbies, and approximately 37,000 square feet of curated amenities, Vista Harbor blends contemporary design, boating access, and rental flexibility in one of Miami’s most connected locations.

A Harbor Lifestyle in the Heart of Miami

Vista Harbor is designed as a private retreat along the river, offering seamless indoor-outdoor living and a true waterfront sanctuary. The development features marina access with private dockage accommodating yachts up to 250 feet, allowing residents to turn the Miami River into a natural extension of daily life.

The project’s bold architecture and waterfront boardwalk create a strong sense of arrival, while the central open receiving area between the towers features soaring 18-foot ceilings, reinforcing its resort-style ambiance.

Residences Designed for Light, Views & Flexibility

Vista Harbor offers studio, one-bedroom, one-bedroom + den, and two-bedroom residences, thoughtfully designed with open layouts and expansive glass windows framing views of Downtown Miami, Brickell, Biscayne Bay, and the Miami River.

Residence features include:

Spacious private balconies

Approximately 9-foot ceilings (with select 12-foot recreation deck units)

Penthouse residences with double-height, floor-to-ceiling windows

Custom Italian kitchen cabinetry

Sub-Zero refrigerator/freezer

Wolf dishwasher, cooktop, and microwave

Kitchen islands or peninsulas (per plan)

Smart keyless entry

Stacked GE washer and dryer

Primary bathrooms with rain shower heads and illuminated mirrors

In addition, Vista Harbor offers minimum 7-day short-term rental flexibility in the West Tower, optional turnkey furniture packages, and on-site rental support services — an increasingly rare combination in Miami’s new construction market.

Resort-Style Amenities & Services

Vista Harbor delivers a full-service lifestyle centered around the river:

Rooftop pool deck with hot and cold plunges

Private cabanas overlooking Downtown and Brickell

State-of-the-art fitness center

Yoga room and relaxing sauna

Outdoor pickleball park with two courts

Business center with co-working stations

Lobby library and wine room

Club room with smart TV and billiards

On-site restaurant and beach club

Front desk concierge

On-site general manager

24-hour security

Marina access along 650 feet of river frontage

Vista Harbor Residences Pricing

At launch, pricing for Vista Harbor Residences is as follows:

Studios starting from the $670,000s

One-bedroom residences starting from the mid-$640,000s

One-bedroom + den residences starting from the mid-$950,000s

Two-bedroom residences starting from the low $1.1 millions, with select corner and water-facing residences priced above $1.2M

Interior sizes currently available range from approximately 497 to 929 square feet, with balconies up to 596 square feet, depending on layout and orientation.

With only 242 residences and strong waterfront positioning, early launch pricing may present a compelling opportunity for buyers seeking riverfront living with marina access and short-term rental flexibility.

Prime Miami River Location

Vista Harbor is located in the heart of Miami along the Miami River, placing residents just minutes from Downtown Miami, Brickell, Midtown, Edgewater, Miami Beach, and the Design District.

By boat, residents can access popular waterfront restaurants such as Bagatelle, Kiki on the River, Seaspice, and Habibi. By car, the property offers quick access to Miami International Airport, PortMiami, the Brightline train station, and the University of Miami Health campus and Jackson Memorial Hospital. River Landing, anchored by Publix and featuring over 315,000 square feet of retail and dining, is also just minutes away.

Vista Harbor Residences & Yacht Club introduces a new standard for Miami River living — combining marina access, modern design, rental flexibility, and resort-style amenities in one cohesive waterfront community.

For current availability, pricing, and floor plans at Vista Harbor Residences & Yacht Club, contact me directly.

Delano Residences & Hotel Miami Sales Launch: 90-Story Branded Supertall Now Selling

A New Era for Branded Luxury Living

The highly anticipated Delano Residences Miami sales launch is officially underway, introducing a 90-story branded supertall to the Downtown Miami skyline. Developed by Property Markets Group (PMG) and branded under the iconic Delano name in partnership with Ennismore and Accor, Delano Residences & Hotel Miami will include 421 fully finished residences and Miami’s first observation sky deck soaring more than 850 feet above the city.

The launch marks one of the most significant branded residential debuts in recent Miami real estate history — offering both flexible short-term ownership options and traditional long-term luxury residences within one landmark tower at 400 Biscayne Boulevard.

Two Distinct Residential Collections at Delano Residences Miami

The Delano Residences Miami sales launch introduces two separate ownership opportunities within the tower:

Select residences include deeded private office suites

Elevated 10-foot ceiling heights

All residences are designed by Meyer Davis and feature floor-to-ceiling glass showcasing panoramic views of Downtown Miami, Biscayne Bay, Miami Beach, and the Atlantic Ocean. Kitchens include custom Italkraft cabinetry, Sub-Zero and Wolf appliances, Waterworks fixtures, smart home technology, and fully built-out closets.

Delano Residences & Hotel Miami Pricing

The current pricing at the time of the Delano Residences Miami sales launch is as follows:

Delano Collection (short-term eligible via the hotel operator)

Suites — from $725,000

1 Bed — from $950,000

1 Bed + Den — from $1,646,000

2 Bed Lockout — from $1,358,000

2 Bed — from $1,601,000

2 Bed + Den — from $2,838,000

Delano Residences

1 Bed — from $1,460,000

2 Bed — from $2,025,000

2 Bed + Den — from $3,115,000

3 Bed — from $3,685,000

With only 421 total residences, early buyers in this sales launch have the advantage of securing preferred floor plans and views before future price adjustments.

Development Timeline & Payment Structure

The Delano Residences & Hotel Miami sales launch follows a structured multi-year development timeline:

10% at Contract (now)

10% in October 2026

10% at Groundbreaking (estimated June 2027)

10% one year after groundbreaking

60% at Closing (estimated 2031)

This phased structure allows buyers to secure a residence today while spacing capital commitments over several years.

Sky-High Amenities & Vertical Programming

Delano Residences & Hotel Miami is programmed vertically to deliver a resort-in-the-sky lifestyle:

10 elevators (residential, hotel, entertaining, and observation deck dedicated access)

4 floors of deeded private offices

9th floor: Event and meeting rooms

15th floor: Main pool deck

17th floor: Signature all-day restaurant

18th & 19th floors: Spa & Wellness – The Source by Delano

78th floor: Rooftop pool

79th & 80th floors: Upper pool deck featuring Rose Bar & Private Members Club

81st & 82nd floors: Rooftop restaurant

83rd floor: Observation sky deck

Residents will also benefit from concierge services, valet, on-site security, housekeeping, pet services, and global Accor ALL Live Limitless Diamond status privileges.

Why the Delano Residences Miami Sales Launch Matters

This is not just another condo release — it’s the debut of a globally recognized hospitality brand in Downtown Miami’s supertall segment.

Key reasons buyers are moving early:

Limited 421 total residences

Flexible short-term rental option in 266 units

Prime Biscayne Bay address

Iconic observation sky deck

Multi-year appreciation window before 2031 completion

Branded residences continue to command strong demand in Miami, particularly those offering rental flexibility and lifestyle programming at this scale.

Secure Your Residence Now

Inventory is now being selected. If you’re considering purchasing at Delano Residences & Hotel Miami, now is the time to review floor plans, pricing, and availability before the first round of price increases.

Contact me today to receive current availability, floor plans, and schedule a private presentation. I can be reached via email at [email protected].

1600 Edgewater: New 33-Story Apartment Tower Moves Forward

The future is unfolding at 1600 NE 2nd Avenue in Miami. Previously home to Battle Racing, the site has been cleared, and construction is advancing on a 33-story tower known as 1600 Edgewater. Despite the name, the site actually sits on the boundary between Edgewater and the Arts & Entertainment District, technically leaning into the A&E District side—Edgewater begins just across the street.

From Demolition to Rising Tower

Replacing the former structure, the tower designed by Kobi Karp Architecture will rise 381 feet, featuring 282 residential units. This mix includes 262 market-rate apartments and 20 affordable units.

Neighborhood Integration & Retail Activation

Although branded “Edgewater,” the project is set to enhance the A&E District’s urban fabric. With 6,615 square feet of commercial space—including a ground-floor retail component and rooftop area—the development aims to invigorate pedestrian life. A structured garage will provide 328 parking spaces.

Progress and What’s Next

Demolition is complete, site clearing is ongoing in preparation for construction. Keep an eye out as this new addition reshapes the skyline, blurring the line between two of Miami’s most dynamic neighborhoods.

House of Wellness Brickell Launches Sales: A 34-Story Wellness-Focused Condo Tower in the Heart of Brickell

A New Wellness-Integrated Condominium Brand Debuts in Miami

North Development has officially launched sales for House of Wellness Brickell, a groundbreaking wellness-integrated condominium concept located at 152 SW 9th Street in Brickell. The 34-story tower will feature 656 condominium residences and introduces a new residential model designed to make wellness-driven, high-design urban living more accessible.

The debut of House of Wellness follows the strong sell-out performance of North Development’s Domus FLATS concept (Domus Brickell Center and Domus Brickell Park), building on that momentum with a brand focused on integrating wellness, hospitality-inspired services, and efficient urban design. Sales are officially underway, with a launch celebration planned in March and the opening of the project’s sales gallery to follow.

Developed by North Development — founded by Oak Capital and Edifica — the project benefits from more than 70 delivered projects and decades of international hospitality and residential development experience. Architecture is led by Studio Mc+G, with interior design by Urban Robot, creating a contemporary and design-forward aesthetic.

656 Residences with Studio, One-, and Two-Bedroom Floor Plans Starting at $390,000

House of Wellness Brickell offers a curated mix of studio, one-, and two-bedroom floor plans, with pricing starting at $390,000. The residences are intentionally compact and efficiently designed, pairing smart layouts with bold contemporary finishes to maximize livability in the urban core.

Homes feature 9-foot-4-inch-high ceilings, finished flooring throughout, porcelain bathroom tile, two-tone cabinetry with terrazzo countertops, and premium appliance packages including cooktop, refrigerator, dishwasher, and speed oven. Select residences will offer polished concrete balconies and sweeping views of the Brickell skyline and Biscayne Bay.

Five stories of private parking, in-house professional management by North Management, and 24-hour concierge and security further elevate the residential experience.

The Integrated Wellness Method: A Structured Approach to Everyday Living

What truly differentiates House of Wellness is its Integrated Wellness Method, a structured, ongoing wellness program built directly into daily life. Each resident begins with a full-body health assessment upon move-in, establishing a personalized baseline. Ongoing evaluations track progress over time, supported by curated services and guided programming.

The wellness program is overseen by a dedicated Lifestyle Director and supported by intelligent technology and a dedicated wellness app. Residents will have access to on-site professionals including nutritionists, personal trainers, physical therapists, massage therapists, estheticians, IV therapy services, and more.

In addition, the building incorporates a building-wide water purification system in partnership with CLEAR, reinforcing the project’s health-forward approach.

22,000 Square Feet of Wellness, Fitness & Lifestyle Amenities

House of Wellness will offer more than 22,000 square feet of dedicated wellness and lifestyle amenities. These include:

State-of-the-art gym

Indoor and outdoor functional training areas

Private personal training room

Outdoor class terrace and cold plunge

Full-service spa with hammam, sauna, and steam room

Treatment rooms

Rooftop pool with panoramic city and bay views

Rooftop club room

Co-working spaces

Social lounge

Juice bar and pantry

Podcast room

Hair salon

Ground-floor urban lounge

Pet-friendly amenities including dog spa and dog park

The amenity program is designed to integrate physical, mental, social, intellectual, and nutritional wellness into daily life — not as an occasional perk, but as a core residential offering.

Prime Brickell Location Adjacent to The Underline and Metromover

Located at 152 SW 9th Street, House of Wellness Brickell sits adjacent to The Underline and the Metromover, and within walking distance of Mary Brickell Village and Brickell City Centre. Residents will enjoy immediate access to dining, retail, grocery stores, cafés, public transportation, and Brickell’s growing pedestrian infrastructure.

A New Chapter for Wellness-Focused Condo Living in Brickell

With pricing starting at $390,000, 656 residences, over 22,000 square feet of wellness amenities, and a structured lifestyle program built into daily living, House of Wellness Brickell represents a new generation of thoughtfully designed, wellness-driven condominium living in Miami.

For buyers and investors seeking a health-focused, design-led residential concept in the heart of Brickell, House of Wellness introduces a brand poised to redefine how urban residents live, invest, and experience well-being.

E11EVEN Hotel & Residences: Closings Start This Month—And 11/11 Would Be Iconic

Closings at E11EVEN Hotel & Residences begin this month, marking a major milestone for this 65-story Park West landmark now in its final phase before full activation. The tower will deliver 479 fully furnished and finished luxury residences ranging from studios to two-bedroom layouts, along with a Limited Penthouse Collection and two Presidential Suites—each featuring a private indoor pool.

While buyers will soon receive their keys, the full 24/11 lifestyle experience—including the hotel, spa, 20,000-square-foot day club, and rooftop restaurant & nightclub—is expected to launch in phases toward year-end. Judging by the current state of the expansive pool deck and entertainment venues, it appears several months remain before full activation. And given E11EVEN’s affinity for headline-making dates—most notably its 11/11/2021 groundbreaking—one could imagine November 11, 2026 as a fitting moment for a grand opening celebration.

A $2 Million Grand Opening Party with a Grammy-Winning Artist?

While there’s no official confirmation on this, I’ve heard from sources that a Grammy-winning artist will be headlining the grand opening party—a grand opening party where the developer is spending $2 million. My sources also shared it’s an artist who absolutely LOVES Miami.

Now, perhaps I’m being a bit hopeful because I’m a HUGE fan, but if I had to venture a guess, I’d put my money on Drake being the headlining performer at the E11EVEN Hotel & Residences grand opening party. He’s a 5-time Grammy-award-winning artist, he absolutely crushes on Miami (often paying tribute to the 305 in his songs), and has performed at E11EVEN Miami seven times, beginning with his debut on New Year’s Eve 2015/2016 and notably highlighting that he created the club’s famous center stage. If my hunch is true, let’s just say this grand opening party will be the must-attend event of 2026!

Riviera Dining Group Elevates E11EVEN: HONŌ Rooftop & Nightclub

At E11EVEN Hotel & Residences, Riviera is set to debut HONŌ Japanese Steakhouse, paired with a rooftop nightclub experience. If MILA transformed South Beach dining, HONŌ could do the same for Park West—bringing world-class culinary programming and a sky-high nightlife concept to the 65th floor.

This isn’t just another restaurant opening. It’s a vertical lifestyle expansion.

Fireman Derek’s Bake Shop—Late-Night Sweet Spot

In even more delicious news, Fireman Derek’s Bake Shop—famous for pies, cakes, cookies, and ice cream—will open its fourth location in the lobby of E11EVEN Hotel & Residences.

With beloved storefronts in Wynwood, Coconut Grove, and Fort Lauderdale, this Park West addition makes perfect sense. Located within the small 24-hour liquor license zone around 11th Street in Park West’s Entertainment District, Fireman Derek’s will be ideally positioned to serve late-night cravings—just steps from the elevator.

For a neighborhood built around nightlife, that’s a strategic move.

E11EVEN: Miami’s Next Lifestyle Magnet

E11EVEN Hotel & Residences is more than a building—it’s a vertical entertainment ecosystem.

A 20,000-square-foot day club with DJ programming.

A rooftop restaurant and nightclub.

A hotel component.

A spa and wellness experience.

A beach club.

Fully furnished residences designed for short-term flexibility.

For years, global jet-setters have flown into Miami just to experience E11EVEN Miami’s ultraclub. Soon, they’ll be able to stay next door—inside a 65-story lifestyle tower built to operate 24/11.

Whether or not 11/11/2026 becomes the official launch date, one thing feels certain:

Park West is about to change.

The countdown begins.

Palantir Moves Headquarters to Miami: What the Big Tech Relocation Means for Florida and Beyond

Palantir Technologies Inc. has officially announced that it will relocate its corporate headquarters from Denver, Colorado, to Miami, Florida — a move that instantly makes headlines across business and tech media. The decision, announced earlier today via the company’s X (formerly Twitter) account, places one of the world’s most influential data analytics and AI firms squarely in the spotlight of the burgeoning South Florida tech ecosystem.

Why Miami? The Rising Appeal of South Florida for Tech Firms

Miami has become one of the fastest-growing tech and innovation hubs in the United States. Once seen as a vacation destination, the region has attracted technology companies, venture capital, and business leaders over the past several years — thanks to business-friendly policies, tax advantages, and a growing entrepreneurial ecosystem. Palantir’s decision to relocate underscores this broader trend, joining other major firms that have either expanded into Florida or shifted key operations there.

Local officials and tech champions argue that Miami’s growth is no accident: the region has pursued economic incentives, lower corporate tax burdens, and a lifestyle appeal that many founders and executives find attractive compared to traditional tech centers like Silicon Valley or New York. Investors and wealthy business leaders — including Palantir Chairman Peter Thiel, who has expanded his own operations in Miami — have been instrumental in this shift.

From Denver to Miami: The Latest Chapter in Palantir’s Journey

Palantir’s headquarters relocation marks the second major corporate move within a decade. The company was previously headquartered in Palo Alto, California, before relocating to Denver in 2020 amid concerns over Silicon Valley’s cultural climate. The recent relocation to Miami reflects a continuation of Palantir’s strategic repositioning in places with favorable business climates and active recruitment of tech leaders.

While the official announcement was brief — “We have moved our headquarters to Miami, Florida,” — details about the impact on staff, office footprint, job creation, or specific Miami office locations have not yet been disclosed. Given the prestige of Miami’s financial district, Brickell, where the upcoming Citadel Tower will rise, or the fast-growing Wynwood tech hub, where 545 Wyn already hosts Sony Music, PwC, Gensler, and Milo—Palantir’s next move could elevate either location even further. It also remains unclear whether the company will maintain a significant Denver presence going forward.

Economic and Community Reactions: Business Boost vs. Local Concerns

The reaction to Palantir’s relocation has been mixed across communities:

Miami and business advocates have celebrated the move as a major win for Florida’s economic development and tech reputation.

Denver community members and critics cited local protests and controversies tied to Palantir’s government and immigration agency contracts as part of the context around the departure.

Economists and analysts will be watching how this move influences job markets, corporate investment trends, and regional competition among U.S. tech hubs.

Palantir’s Strategic Future: Growth, Innovation, and Market Trends

Palantir remains a major player in data analytics and government contracting, with a portfolio of software platforms used by governments and corporations worldwide. Moving the headquarters to Miami positions the company in a region actively pursuing innovation and business growth, potentially opening new avenues for partnerships and talent acquisition.

As Miami solidifies its status as a technology and business magnet, analysts see Palantir’s move as part of a larger story: the ongoing reshaping of where tech firms choose to locate and scale. This has implications for investors, employees, local economies and the broader narrative of American tech innovation in 2026 and beyond.

A Defining Shift

Palantir’s announcement that it has moved its headquarters from Denver to Miami is a defining moment for the company and significant validation of Miami’s rising tech stature. While many questions remain — including specifics about operations, job impacts, and longer-term strategy — today’s news highlights continuing shifts in corporate geography driven by economic incentives, lifestyle choices, and industry evolution.