Miami & Miami Beach Condo Trends – July 2009

I collected the following figures last Thursday night on July 23, 2009. It has been about six months since I last published inventory numbers for condos in Miami-Dade County. The last Miami & Miami Beach Condo Trends post was published on January 19, 2009.

As many of you read earlier today, the Case-Shiller price index rose on a month-to-month basis for the first time in 3 years. 13 of the 20 cities in the index showed month-over-month price gains in May when compared with April 2009. However, Miami was not one of the 13 cities to show an improvement in prices. Home prices in Miami saw a decrease of .8 percent during that period.

There may not have been an increase in home prices in Miami but the figures below show a major improvement in the number of closed condo sales in the previous six months when compared to the closed condo sales in the six months prior to January 2009. For example, there were 3,551 closed condo sales in the six months leading up to January 2009 compared to the 5,007 closed condo sales that occurred within the past six months. That’s an increase of 41 percent. The number of closed condo sales in Miami improved approximately 39 percent while closed condo sales in Miami Beach increased about 20 percent. As a result, the condo supply numbers for each showed considerable improvements as well.

View the entire workbook for this month’s Miami & Miami Beach Condo Trends. The various spreadsheets and graphs are found at the bottom.

Below, you will find the Miami-Dade County condo inventory and supply figures for July 2009:

The following statistics encompass only those condos located throughout Miami (not other areas of Dade County such as Miami Beach, Aventura, Sunny Isles Beach, etc.):

The following statistics encompass only those condos located throughout Miami Beach:

This has been a very atypical year for real estate sales in South Florida. In most years, the vast majority of closed condo sales occur in the Winter months when snowbirds flock to Florida to shop for a vacation home to escape the dreaded cold. However, this past Winter season was unusually slow due to a number of reasons such as the paralyzing fear in the economy and a lack of financing. After the first 3 months of the year, I personally felt that 2009 was shaping up to be my worst year in real estate. However, at the beginning of April, business began to show life again. In fact, activity has drastically improved to the point where 2009 could end up being one of my best years. I personally feel that the Miami condo market is within 2-3 months of reaching the bottom. That’s in no way saying that prices will begin to increase soon after. The overall market needs to move sideways for at least the next 12-24 months before we see any significant increase in sales prices.

Top 5 Distressed Condo Sales Closed in May 2009

Below, you will find what I believe to be the five best condo deals of the 46 distressed sales that closed in the month of May in the MLS located in Brickell, Brickell Key, Downtown Miami and the Arts District. I think the distressed condos that closed in the month of May were better deals than what we have seen in previous months.

- Jade Brickell – unit 1002 – 2 bedroom/2 bath (1,529 square feet) – This unit sold for $375,000, or $245 per square foot, on May 15, 2009. Short Sale

- Courts Brickell Key – unit 1909 – 3 bedroom/3 bath (1,488 square feet) – This unit sold for $350,000, or $235 per square foot, on May 20, 2009. Short Sale

- Skyline on Brickell – unit 306 – 2 bedroom/2 bath (1,367 square feet) – This unit sold for $349,000, or $255 per square foot, on May 8, 2009. Foreclosure

- Skyline on Brickell – unit 1512 – 2 bedroom/2 bath (1,367 square feet) – This unit sold for $305,000, or $223 per square foot, on May 18, 2009. Short Sale

- One Miami – unit 3916 – 1 bedroom/1 bath (846 square feet) – This unit sold for $150,000 or $177 per square foot, on May 27, 2009. Foreclosure

Runner-ups:

- The Mark on Brickell – unit 1001 – 2 bedroom/2 bath (1,200 square feet) – This unit sold for $205,000, or $171 per square foot, on May 22, 2009. Foreclosure

- 1800 Biscayne Plaza – unit 203 – 2 bedroom/2 bath (1,057 square feet) – This unit sold for $120,000, or $114 per square foot, on May 01, 2009. Short Sale

- Cite on the Bay – unit 2213 – 1 bedroom/1 bath (795 square feet) – This unit sold for $100,000, or $126 per square foot, on May 13, 2009. Foreclosure

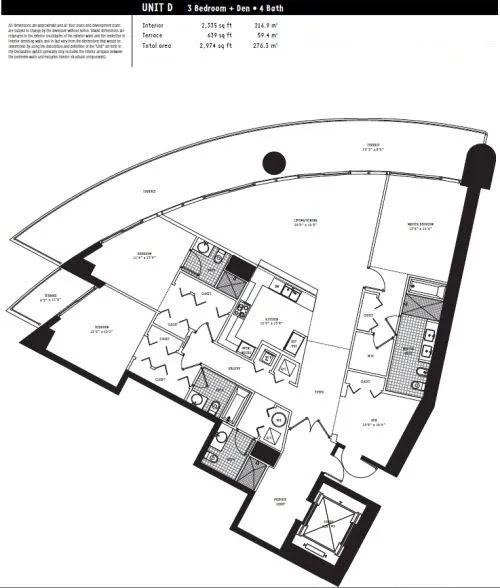

900 Biscayne Bay 06 Line

It’s no secret that 900 Biscayne Bay is my favorite building of all the condo developments in Miami that have been completed within the past three years. When I show properties to clients who wish to view 900 Biscayne Bay as well as other condo buildings, I tend to leave 900 Biscayne Bay last. Otherwise, everything else will look second-rate by comparison if I were to show it first. I guess it’s my “leave the best for last” mentality. 900 Biscayne Bay is in a league of its own. Building security is some of the best in Miami and the overall quality of the development and amenities is second to none. Additionally, valet parking is currently complimentary for a second vehicle as well as for resident guests. View a photo tour of 900 Biscayne Bay.

That being said, of all the floor plans at 900 Biscayne Bay, the 06 line is the one that excites me most. It’s a 3 bedroom + den/4 bath unit with 2,335 square feet of interior and 639 square feet of exterior. A few days ago, I showed unit 3006 at 900 Biscayne Bay to a client looking for a 3 bedroom rental. Below, you’ll find a photo tour of that condo as I walked throughout its spacious footprint. Notice the sizable foyer as you enter the condo from its private elevator, the top-of-the-line stainless steel appliances, deep terraces and amazing views. (Asking price to rent this unit is $4,200 per month.)

Foyer

Entrance

View

Kitchen and Entryway

Kitchen

Kitchen

Master Bedroom

Master Bathroom

Second Bedroom

Second Bathroom

Third Bedroom

Third Bathroom

Den

Terrace

View

900 Biscayne Bay Condos For Sale

900 Biscayne Bay Condos For Rent

Marina Blue Penthouse

Just wanted to share some great pictures that I shot earlier today of a 2,703 square foot penthouse at Marina Blue. All penthouse condos at Marina Blue have 20-foot ceilings.

Fannie Mae Approved Condo Buildings in Florida

As of June 1, 2009, Fannie Mae updated their website to reflect the condo developments in Florida that are now approved for financing.

The following is a list of recent condo developments in South Florida that are now Fannie Mae approved:

View the full list of Fannie Mae approved condo developments in Florida.

Views from the 54th Floor at 50 Biscayne

Earlier this afternoon, I showed a 2 bedroom + den/2 bath rental at 50 Biscayne on the 54th floor. I wanted to share the pictures below with those who haven’t had a chance to visit an east facing unit at 50 Biscayne. Asking price of the 2 bedroom + den with 1,357 square feet is $2,600 per month.

Northeast view from the 54th floor at 50 Biscayne:

East view from the 54th floor at 50 Biscayne:

Southeast view from the 54th floor at 50 Biscayne:

South Florida Luxury Condo Short Sales

Currently, there is only one foreclosure condo listed in the MLS that is priced at $1M or above. That is a 3 bedroom/4.5 bath double corner unit at The Setai South Beach with 3,691 square feet of interior space. The list price is $4.2M, or $1,138 per square foot. However, there are currently 48 short sale condos listed in the MLS priced at $1M or above. Below is a list of what I feel are the 10 best luxury short sale condos that are currently available:

- Aqua Allison Island #6111 – Asking $1.69M. Property was purchased for $3.15M in June 2005.

- Mosaic #TH-3 – Asking $1.7M. Property was purchased for $3.2M in February 2007. Bank approved at $1.7M.

- Oceanside Fisher Island #7941 – Asking $1.85M. Property was purchased for $3.9M in November 2006.

- Oceanside Fisher Island #7735 – Asking $1.85M. Property was purchased for $2.4M in September 2005.

- Oceanside Fisher Island #7761 – Asking $1.95M. Property was purchased for $3.2M in September 2005.

- The Bath Club #1004 – Asking $1,999,999. Property was purchased for $3.5M in January 2007. Bank approved.

- Turnberry Ocean Colony #2804 – Asking $2,295,000. Property was purchased for $3.27M in January 2008.

- Bayview Fisher Island #5123 – Asking $2.3M. Property was purchased for $3.7M in March 2007.

- Acqualina #4201-2 – Asking $2.8M. Sales history not found.

- Oceanside Fisher Island #7821 – Asking $2.8M. Property was purchased for $3.92M in November 2006.

Top 5 Distressed Condo Sales Closed in April 2009

Below, you will find what I believe to be the five best condo deals of the 42 distressed sales that closed in the month of April in the MLS located in Brickell, Brickell Key, Downtown Miami and the Arts District.

- Emerald at Brickell – unit 2201 – 2 bedroom/2.5 bath (1,594 square feet) – This unit sold for $306,000, or $192 per square foot, on April 30, 2009. Foreclosure (#1 despite the high HOA fees)

- The Club at Brickell Bay – unit 2604 – 1 bedroom/1 bath (825 square feet) – This unit sold for $110,000, or $133 per square foot, on April 9, 2009. Short Sale

- One Miami – unit 3215 – 2 bedroom/2 bath (1,145 square feet) – This unit sold for $255,000, or $223 per square foot, on April 13, 2009. Short Sale

- Skyline on Brickell – unit 1912 – 2 bedroom/2 bath (1,367 square feet) – This unit sold for $325,000, or $238 per square foot, on April 17, 2009. Foreclosure

- Brickell on the River North – unit 1007 – 1 bedroom/1 bath (757 square feet) – This unit sold for $145,000 or $193 per square foot, on April 17, 2009. Foreclosure

Runner-up: Vue at Brickell – unit 2108 – 1 bedroom/1 bath (838 square feet) – This unit sold for $94,000, or $112 per square foot, on April 29, 2009. Foreclosure

Unit 1508 at Brickell on the River North Revisited

Towards the end of February, I wrote about a 2 bedroom/2 bath condo foreclosure at Brickell on the River North that had recently been listed at the time. The condo was listed for $159,000, or $151 per square foot. The 2 bedroom was priced below recently closed 1 bedroom condos at Brickell on the River North and, as a result, attracted the interest of many buyers. From speaking with the listing agent in February, I learned that he had received over 30 offers for the condo. The unit closed on April 3, 2009 for $236,000, well above asking price.