Icon Brickell Developer Agrees to "Friendly Foreclosure"

Yesterday, The Related Group and its lenders agreed to a “friendly foreclosure” for Towers 1 and 2 of Icon Brickell. This video provides our commentary as well as the details pertaining to the agreement.

Miami Real Estate Review – Episode One

Over the past couple of months, we’ve been working on a project that we hope will separate ourselves from other South Florida Realtors and allow us to disseminate market news and information to our audience in an efficient and innovative way. The video that you see below is the result of an idea that was born a few months ago. We decided to launch a real estate video show. This initial video provides an overview of what we have in mind for our video show and demonstrates how we’ll utilize the iPad in conjunction with it.

Atlantis on Brickell Amenities Video

For those of you not familiar with Atlantis on Brickell, I’ve included a video tour below of the amenities and common areas. Atlantis on Brickell was completed in 1982 and is well recognized for its colorful and unique architecture. This iconic building is well remembered as being featured in the opening credits of the 1980s hit TV show, Miami Vice. The steps to the entrance of the lobby of Atlantis on Brickell was also featured in the 1980s cult classic Scarface. Welcome to Atlantis on Brickell:

Miami-Dade County Pending Home Sales Soar

In today’s edition, The Miami Herald reported that April 2010 pending home sales in Miami-Dade County are up 71 percent year over year and up 6.6 percent since the prior month. The data was released Tuesday by the Realtor Association of Greater Miami and the Beaches.

900 Biscayne Bay 06 Line Video

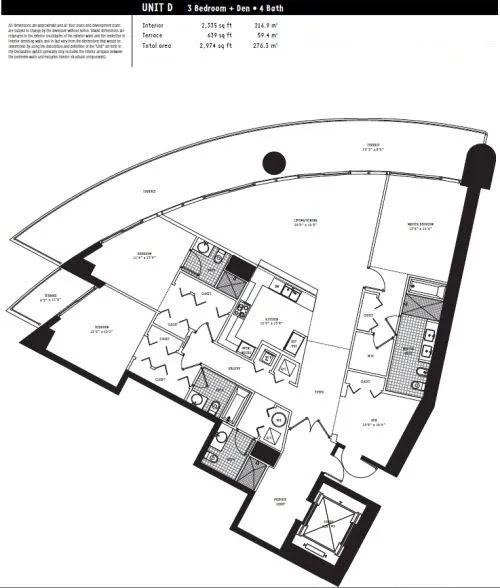

Now that we’ve seen a video of the amenities at 900 Biscayne Bay, let’s take a look at an actual unit in the building. The video above will show you an 06 line located on the 33rd floor. This is one of my favorite floor plans at 900 Biscayne Bay. It’s a 3 bedroom + den/4 bath condo with 2,335 square feet of interior and a 639 square foot terrace. The unit has a direct view of Biscayne Bay the moment you walk through the double entry doors from your private elevator.

900 Biscayne Bay condos still remains my favorite of all of the condominium high-rises built in Miami within the past ten years. The quality of the building and units is unmatched and it has some of the most spectacular amenities of any building that I’ve encountered. I think after viewing the high definition video below you’ll see exactly why I feel that way.

At this time, about 80 percent of the units at 900 Biscayne Bay have closed or are under contract. The building is Fannie Mae approved. Contact us at 305-428-3860 if you have an interest in viewing 900 Biscayne Bay in person or would like to discuss developer inventory.

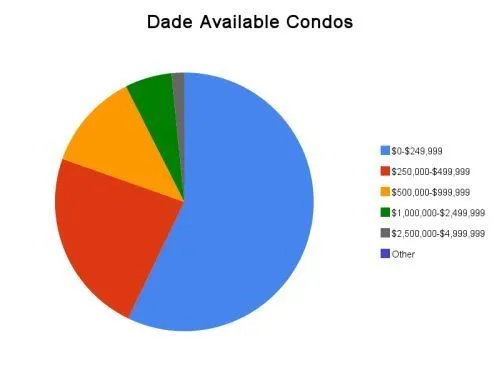

They say numbers don’t lie. If that be the case, one message of truth shines through in the inventory figures below when compared to the ones I calculated exactly nine months earlier for Miami-Dade County condos: sales up, supply down. I compiled the figures below on April 22, 2010 from the MLS in the exact same manner as I had the night of July 23, 2009. Below, you will find three sets of spreadsheets and graphs: the first pertaining to the inventory of condos throughout Miami-Dade County; the second to those residing only in Miami while the third concentrates on those residing in Miami Beach.

Once again, I divided the supply figures into seven price ranges and included only sales that have closed within the past six months. The last three columns show the percentage change in those statistics when compared to those published nine months earlier for July 2009. It should be rather apparent, with a few exceptions, that the overall pattern is that condo inventory has decreased and closed sales have increased quite considerably within the past nine months. For example, overall condo inventory in Miami-Dade County has decreased 13.78 percent while closed sales have increased 19.23 percent during that time frame which led to a 27.69 percent decrease in the overall months of supply.

The figures in the images below may be a bit difficult to read so I also published the workbook for this month’s Miami & Miami Beach Condo Trends in its entirety. Be sure to check it out. The worksheet and graph tabs can be found along the bottom of the workbook.

Below, you will find the Miami-Dade County condo supply and sales figures for April 2010:

The following statistics encompass only those condos located throughout Miami (not other areas of Dade County such as Miami Beach, Aventura, Sunny Isles Beach, etc.):

The following statistics encompass only those condos located throughout Miami Beach:

Market pessimists will likely argue that the statistics above do not incorporate developer inventory. Commonly known as shadow inventory, developer inventory is typically not recorded in the MLS. However, these people need to bear in mind that closed developer sales also are not included in the figures above. Obviously, shadow inventory was a bigger problem nine months ago than it is today. A more valid argument should point to the home buyer tax credit being the catalyst that increased sales within the past nine months. Personally, however, I feel that the the home buyer tax credit has had a greater impact on the single family home market than the condo market. It has played a very insignificant role in our business and I have spoken to other real estate agents who specialize in condominiums who have encountered the same. With the home buyer tax credit expiring this Friday, we should be able to see within the next three months how instrumental of a role it has played in the increased sales numbers we’ve witnessed.

Marina Blue Receives Fannie Mae Approval

On April 20, 2010, Marina Blue received a letter from Fannie Mae stating that the building has been accepted under Fannie Mae’s Special Approval Designation for twelve months. Qualified buyers will now be able to obtain financing using a Fannie Mae conventional loan.

Potential buyers may want to take a look at unit 2203 at Marina Blue. It’s a 1 bedroom + den/1.5 bath condo with 943 square feet of interior, 9-foot ceilings and a balcony that stretches the length of the unit. The condo offers views of Biscayne Bay, Key Biscayne, the Miami Beach skyline and Downtown Miami. At an asking price of $300,000, it is being offered at the lowest price per square foot of any 1 bedroom condo at Marina Blue currently active in the MLS. Take a look at the video tour below.

Best Priced 2 Bedroom at Marina Blue – $390,000 – Video

Take a look at the video below to view the best priced 2 bedroom currently available at Marina Blue. This 2 bedroom/2 bath condo has 1,198 square feet of interior, 138 square feet of balcony, 9-foot ceilings, tiled flooring throughout, stainless steel kitchen appliances, Wenge built-in closets in both bedrooms, washer/dryer and 1 assigned parking space. The asking price is $390,000.