Developers Offering Year-End Incentives to Close Out Projects

In an effort to hold the attention of buyers and sell as many apartments as possible before the end of 2015 developers are coming out with attractive incentives packages to help buyers decide to act now and close out their projects Here are some of our favorite incentives from buildings that are currently under construction and selling pre construction residences

Brickell Heights Related has lowered the down payment requirement to 30 from the original 50 Prices of remaining inventory start in the $400000s

SLS Lux All of the condohotel apartments are currently under contract but the developer is offering upgraded kitchens on the remaining condo residences and 30 down payment The penthouse collection has recently been released and sales are almost finished Prices start in the $600000s for the remaining units

Paraiso Bayviews All four towers of the Paraiso development are currently under construction and Paraiso Bayviews is 95 sold For select apartments the developer is offering a finishes package with porcelain flooring throughout The prices currently start in the mid $500000s up to the high $600000s and penthouses are priced between $639900 to $175MM The developer has not officially offered deposit flexibility but has indicated that it is possible on a case by case basis

Hyde Midtown The construction of Hyde Midtown has only just started in recent months but close out is fast approaching Prices on remaining inventory start in the $400000s and the sales team has offered some flexibility on the 30 down payment on a case by case basis

We were very happy to see these flexible down payment options as it will make new condo purchases more accessible to those who hope to live in the apartments The incentives also help to allow for the possibility of financing the condo purchases which many people have inquired about yet been unable to easily attain until now

Let us know if you or someone you know is interested in more information on these or other developments We will have team members in Miami during all of the holidays and until the end of the year to help visitors by appointment

Real Estate Connect – The Housing Debate: Bulls vs. Bears

I’m so glad that Brad Inman, of Inman News, posted the following video. This was hands down the most interesting discussion that I attended this past week.

The speakers on the stage were made up of the following:

- Andrew Ross Sorkin – Assistant Editor, Business & Finance, Chief Mergers and Acquisitions Reporter of the New York Times

- Dottie Herman – President & CEO of Prudential Douglas Elliman

- Barry Ritholtz – Chief Market Strategist, Ritholtz Research & CEO; Director of Equity Researh, Fusion IQ

- Noah Rosenblatt – Founder of Urbandigs.com/Licensed Real Estate Sales Person, Citi-Habitats

- Professor Nouriel Roubini – Co-founder & Chairman of RGE Monitor; Professor of Economics at New York University’s Stern School of Business

The most colorful speaker was by far Professor Nouriel Roubini. There were a few times where everyone in the room was saying to each other “I can’t believe he just said that”. He cracked me up because he was so matter-of-fact. That’s one person that I’d love to have a conversation with over lunch. Barry Ritholtz and Noah Rosenblatt were also very insightful.

I also love what Barry Ritholtz says about “anchoring”. Sellers need to detach themselves from anchoring and either delist their properties or be realistic in pricing their properties. What he has to say is so true. I’ve been saying this for months. The real estate market needs to hit the reset button.

Rumor Mill on the Streets of Manhattan

I arrived at La Guardia Airport in New York City on Tuesday afternoon. The good news was that the weather was fantastic. It was in the high 60s, which was unprecedented in New York City for the month of January. The weather was just what I needed after arriving in Chicago last week on the coldest day of the Winter season (I think it was something like 15 degrees below zero with wind chill). Brrrrr!!! In fact, the first thing I did when arriving in Chicago was to go to Target and buy some long underwear. It was that freakin’ cold! I used to live in downtown Chicago for 4 years so I should know cold, but that day was damn cold! Maybe living in Miami for so long has made my blood thin out a bit or something.

My arrival in New York City, however, soon turned sour after learning that my luggage was lost by American Airlines. Regardless, I checked into my hotel and tried to make the best of my trip. My luggage did finally arrive at 3am that night (the next morning).

Last week, I wrote a post mentioning that I would be in New York City from January 8-11 for the Real Estate Connect NYC 2008 Conference. I was contacted by one hedge fund analyst and two investment groups that wanted to meet me while I stayed in New York City. They each had an interest in the Miami condo market.

Today, I attended the first day of the Real Estate Connect Conference and listened to a few industry leaders speak about the market. I also picked up some great information in conversations with people in the hallways as well as the hedge fund analyst that I met with later in the evening.

Okay…enough with the boring stuff. Let’s get to the goods! The following is the rumor mill that was revealed to me throughout the day. This is just what I’ve heard. I am in no way saying that the rumors are true (although these rumors came from accredited sources).

- WCI will declare bankruptcy within the next two weeks. Shares of WCI, the developer of One Bal Harbour, dropped 52.98% today on worries that WCI will declare bankruptcy. Standard & Poor affirmed WCI’s junk rating status and provided a negative outlook for the company. (Can you say “Pink Sheet”?) WCI was provided an extension until January 16, 2008. That’s a very short extension. My source disclosed to me tonight that the bank is probably finally realizing that it is in their best interest to pursue bankruptcy proceedings rather than delay the inevitable. The mathematics makes sense for the bank to do so. Most banks loaned about 65 percent of the total construction costs. As of right now, according to public records, WCI has closed 50.3 percent of the condo units at One Bal Harbour. If I were the bank holding onto the construction loan for One Bal Harbour, I would foreclose on this development immediately. The lender could at least offset their other losses with the gains they may realize with the sale of the defaulted units at One Bal Harbour. They know that it’s a strong development…I know that it’s a strong development. Until the investment funds step in, however, there’s still a lot of risk.

- Marina Blue closings have been pushed back 2 months and possibly even longer. I heard this rumor when I was in Miami on Monday but I didn’t accept it until tonight. I’ve heard that Marina Blue has no clue when closings will begin. Somebody please tell me that I’m wrong! I’ve heard this one from multiple sources though.

- Opera Tower is delaying closings another month. I’ve heard this one from multiple sources as well. What the hell is going on with this development? It keeps delaying its closings. Weren’t closings supposed to realistically begin around September? I was recently misquoted about Opera Tower in the papers. I was quoted as saying something along the lines that Opera Tower will have a 50 percent default rate. I actually said that Opera Tower will have at least a 50 percent default rate. Just my opinion though. Also, just my opinion is that this development is doomed. There’s a large lawsuit against the developer of Opera Tower. You may think I’m crazy but I think in six months my 50 percent default rate for Opera Tower will be considered an overzealous prediction.

- Here’s the big one. Countrywide Financial Corporation is going to declare bankruptcy within the next three weeks. Countrywide has lost about 44 percent of its value within the past 5 days. Rumors around Wall Street are that this turkey is just about roasted and ready to be eaten. We should see this one fall soon…and it’ll make a huge thud on the Street when it does.

- This one isn’t so much a rumor. Quantum on the Bay began closings and the development isn’t even close to being completed. (From what I’ve heard) TCO was granted in order to avoid a lawsuit pertaining to how long the development took to be completed. My guess (and only my guess) is that some money (maybe a lot) was transferred between the developer and city to get the TCO done to avoid lawsuits against the developer.

Miami & Miami Beach Condo Trends – November 2007

I’m going to start including a monthly condo trends report. My hope is that it will help to shed more light on the current state of the market. It is likely to be my most followed monthly piece. After the new year it, along with some other newly added statistics such as a rental market index, will become “premium” content. Just wanted to give you all the heads up. I just finished compiling the numbers and I was pretty shocked.

I basically wanted to find out how many months of inventory we have in Miami and Miami Beach. I created a report for Miami-Dade County, one for Miami and one for Miami Beach. I broke each report down to various price ranges to figure out which category has been affected the most. I took closed sales for the month of October and compared it to the inventory that is now available. Below you will find the numbers for Miami-Dade County:

As you can see Miami-Dade County has about 55 months, or 4.58 years, worth of inventory. I wanted to see how much of this supply resides in Miami compared to Miami Beach. Below you will find the numbers for Miami:

Miami currently has a 48 1/2 month, or approximately a 4 year, supply of condos. That’s actually much lower than I expected. However, keep in mind that there are thousands of condos that will come onto the market within the next 24 months. In fact, in July, I calculated that a little over 16,000 condos would hit the market within the next 19 months in the neighborhoods of Brickell Key, Brickell, Downtown Miami, Park West and the Performing Arts District. Probably about 1,500 or so units have hit the market since I wrote that post. If you add 14,500 units to the Miami figures above then we’re looking at close to a 10 year supply. Now that’s quite shocking!!!

Let’s take a look at the Miami Beach figures:

I was surprised to learn that the supply of Miami Beach condos is higher than that of Miami’s. The number of new condos coming onto the market, however, in Miami Beach pales in comparison to the new condos scheduled to hit the market within the next two years. My guess is that about 1,500 units will hit the Miami Beach market in that time which would put it at around an 8 year supply. Still pretty shocking given that it’s Miami Beach! I was equally shocked by the low number of closings in the $500,000-$999,999 price range. That appears to be a problematic price range if you’re a condo owner looking to sell somewhere in that range.

Despite a number of news stories that have hit the press lately, it looks like the ultra-luxury ($2.5M+) market isn’t moving. It has very few available listings compared to the other categories but it had basically no closed sales in October. There were a total of two in all of Dade-County. Both were located in Bal Harbour.

I receive a lot of monthly phone calls from investors who are waiting for the market to bottom-out. They all want to know when is the “right” time to buy into the South Florida condo market. I’m hoping that a report like the one above can help me pinpoint when that time might be.

A recent Fortune magazine article entitled, “Real Estate: Buy, Sell, or Hold?”, said the following:

The combination of steep discounts to move inventory and a stream of new communities built at a lower cost will keep prices far below their peak levels in the boom towns. And they’ll keep falling until builders work off the massive inventories. The tumbling prices of new homes, in turn, will put enormous pressure on the far bigger existing-home market, already under stress from two desperate groups of sellers, investors and banks. Hence, the adjustment needed to bring the ratio of prices to rents into alignment will happen far faster than in most housing downturns. “In the most vulnerable places in California and Florida, it’s highly possible that most of the correction will happen by the end of 2008,” says (Mark) Zandi, (chief economist at Moody’s Economy.com).

The article was mainly discussing single-family homes but I think the same holds true for the condo market. The Miami condo market is likely to drop lower, on a percentage basis, than other major U.S. cities but I agree with Mark Zandi that the market here will be quicker to correct itself because of the high number of foreclosures and defaults that we are likely to see. 2008 will be a time of readjustment. I’m looking quite forward to it.

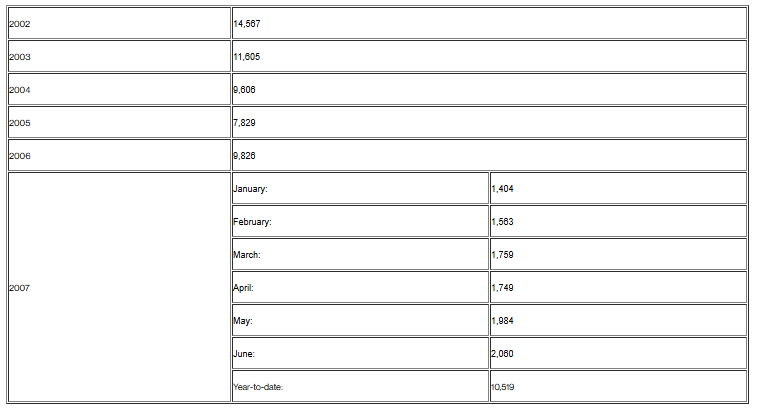

Miami-Dade Foreclosure Filings Since 2002

A friend of mine passed along the following statistics that were disclosed by Miami-Dade County. I found the statistics to be quite compelling and felt that my readers might find these numbers to be of interest as well. It is worthy to note that these numbers indicate that we are on pace to surpass the highs in foreclosure filings in 2002. That isn’t a bit surprising given the state of the real estate market.

These numbers only represent a mid-half report for 2007. As a sizable amount of adjustable-rate mortgages are scheduled to reset in the following three months, I’m sure that we’ll surpass previous year foreclosure filings. Foreclosures usually take about 6 months, so I’m expecting that foreclosure filings will peak in 2008.

| 2002 |

14,567 |

| 2003 |

11,605 |

| 2004 |

9,606 |

| 2005 |

7,829 |

| 2006 |

9,826 |

| 2007 |

January: |

1,404 |

| February: |

1,563 |

| March: |

1,759 |

| April: |

1,749 |

| May: |

1,984 |

| June: |

2,060 |

| Year-to-date: |

10,519 |

More Than $50B in Adjustable-Rate Mortages to Reset in October 2007

An article entitled, “Mortgage Resets: Record Bill Coming Due,” was published today on the CNN.com website. It provides great insight as to how the real estate market can go from bad to worse in upcoming months. Hybrid adjustable-rate mortgages, or ARMs, were a popular financing option for homebuyers in 2004 and 2005. Many of these homeowners will see an increase in their mortgage payment of over 30 percent once those resets occur. That is a significant increase which could lead to a tidal wave of late payments and, eventually, foreclosure for a large number of homeowners.

Historical Real Estate Roller Coaster Adjusted for Inflation

I’ve seen the following video several times in the past, but recently Wellcomemat added a chapter menu to the video to aid those impatient people (such as I). The video will display the ups and downs of the real estate market since 1890, plotted as a roller coaster ride. It takes a while to download all of the chapter menus but it is worth the wait. Jump to 1970-1990 to see the type of plunge that the United States real estate market took back then. Notice the year markers in the lower right hand corner. Continue the ride to see where the market is now, and to get an idea of where Miami real estate may be headed.

Luxury Homebuyer Trends

REAL Trends, Inc. recently reported the results of The 2007 Membership Survey of Luxury Housing Market Trends. I found the results to be quite interesting.

- The largest percentage of luxury homebuyers falls into the 40-50 age group (48%) followed closely by the 50-65 age group (44%).

- The most common occupation of luxury homebuyers is that of an entrepreneur (51%), followed by large business executive (46%) or medical doctor (24%).

- The number one service affluent homebuyers are interested in receiving from their luxury home specialist is help in finding a home (86%) followed by help in managing the transaction (56%) and expert counsel during a negotiation (43%).

- The typical luxury homebuyer makes a large cash investment in his or her home purchase amounting to more than a third of the overall purchase price. In many metro markets this would exceed a quarter of a million dollars. This compares to the median amount financed by all buyers in 2006 of 91 percent of the purchase price.

- The average luxury homebuyer spends 11 weeks looking for a home and views 12 homes.

- Luxury homebuyers on average search for homes consisting of at least 3,500-4,000 square feet, with 4-5 bedrooms and 3-4 bathrooms.

- The amenities most popular with luxury homebuyers include gourmet kitchens (95%), master bedroom suites (86%), specialty construction items (66%), high-end appliance packages (64%), home office suites (58%) and home theater rooms (55%).

- The average listing price for luxury homes is nearly $900,000 dollars, or more than four times than the median price of all U.S. homes as of May 15, 2007 ($212,300).

Source: REAL Trends, Inc.

Flashback to 1983

Yesterday I was given the link to an interesting news article that was published in The New York Times on March 21, 1983 entitled, “Auctioneer’s Gavel Finally Moves Luxury Condominiums in Miami”. You can find that story below or by clicking the link above:

Three hundred people spent a sunny afternoon today in the shade of a big white tent listening to the patter of an auctioneer hawking luxury condominiums, many of which were sold at discounts of 30 to 45 cents on the dollar.

As the market for luxury condominiums remains soft, more developers are taking this route to dispose of their inventory to cut their losses.

About 60 units were sold for $125,000 to $190,000 in the first day of a four-day auction at Biscayne Cove, a luxury high-rise complex overlooking blue waters, nestled among other luxury dwellings in North Miami Beach.

“We decided to auction off and give the people a bargain,” said Morton Littlemen, a representative of the developers. “We want to give the people a condominium they can afford to own.”

One two-bedroom penthouse that was originally offered for $248,000 was sold for a high bid of $150,000. Condominium prices in the two-building complex range from $100,000 to $334,000.

Biscayne Cove is the fifth such auction that Martin Higgenbotham, an auctioneer, has handled in the last year for the developers, subsidiaries of Cadillac Fairview Corporation and Southeast Florida Properties. It is, Mr. Higgenbotham said, the largest single condominium auction in Florida: 225 units on the block at a value of $46 million. It is more than the total of 152 units sold at the other four complexes in Miami Beach and Hallandale.

The condominium auction business has been “heavy,” Mr. Higgenbotham said. In the last 12 months his company has sold about 1,000 condominiums at auction. Previously it handled 250 units in an average year.

The decision to auction the properties was not taken lightly, according to Lewis Goodkin, a real estate consultant whose firm conducted a marketing study for Biscayne Cove and recommended the auction for fast results. “The purpose is, let’s get out of this stuff and let’s get out of it fast,” he said. Normal advertising and deep discounting is “like a prolonged agony.”

Mr. Goodkin’s study concluded that, even under good conditions, it would take three years for the market to absorb existing inventory and that it did not pay for developers to hold onto the property. “We have in Miami today the most overbuilt luxury condominium market in the country,” Mr. Goodkin said.

He foresaw more auctions of this magnitude. “When the last recession hit us, we had a lot more inventory, but the inventory was more affordable,” he said. “A tremendous number of the public could respond. It could be absorbed. Today, our big invetory is in the luxury ranges where the market is not deep and you don’t have the response from the South American markets because their economy is weak or low.”

While the glut is most severe in Miami, it is not exclusive to this area, Mr. Goodkin said.

Is this the fate of the luxury condo units that will come to market in the next 12-24 months in Miami? 20,000! That is the number that has been thrown around for the number of new condo units that will close in 2007 and 2008. It is difficult to imagine that a supply of that magnitude can be absorbed in such a short period of time. It will be interesting to see what percentage of people walk away from deposits rather than close. If a significant portion walk then developers will likely be forced to take immediate action which could recall memories of 1983.