1100 Millecento Residences – A First Look

If all goes according to plan, Related Group will follow pre-construction sales of myBrickell with the launch of 1100 Millecento Residences, a proposed 382-unit condo development to be located directly east of the north tower of Axis at 1100 S Miami Avenue in Brickell. Designed by world-renowned architect Carlos Ott, the development formerly known as myBrickell 2 will rise 42 stories and include street-level retail space.

Pre-construction sales information has yet to released for 1100 Millencento Residences but expect an announcement soon given the level of demand for Miami condos at this time and the fact that Related Group is close to selling out myBrickell.

The Mark on Brickell 3 Bedroom – $365,000

If you are in the market for a 3 bedroom condo in Brickell but on a limited budget, you might want to consider this property at The Mark on Brickell. I came across it while conducting a search on the MLS on behalf of a client and was surprised at the price. It’s a 3 bedroom/2 bath condo with 1,470 interior square feet and travertine and wood flooring throughout. The asking price is $365,000, or $248 per square foot, which is an exceptional value to be in a waterfront building in Brickell. The unit does not have a water view but one should not be expected at this price point. Expect to pay at least $100,000 more for a 3 bedroom in Brickell if you require a water view. This condo is located on the 6th floor with direct access to the pool deck which does offer panoramic views of Biscayne Bay. The unit is currently tenant-occupied but the lease ends next month.

Miami Condo Prices on the Rise

Everyone seems to be in agreement nowadays that the Miami condo market has fully recovered. In fact, not only has the condo market recovered but prices are now on the rise. A recent report released late last month by the Miami Association of Realtors showed that the median sales price for condominiums in Miami rose a remarkable 36 percent year-over-year in January. The average sales price for Miami condominiums increased 45.2 percent in the same time period.

Existing condo inventory continues to be absorbed at a rapid pace and new inventory won’t hit the market until at least the second half of 2013 when myBrickell is scheduled for completion. Pre-construction sales have gone remarkably well at myBrickell with over 85% of the units now under contract. Meanwhile, pre-construction sales at Brickell House, a 374-unit luxury high-rise scheduled for completion in 2014, has experienced similar success with over 60% of the units now under contract. Other condo projects have been approved by the city for development but sales have yet to be launched despite an overwhelming demand from foreign buyers.

Don’t take my word for it though. Here are a few major news sources who have recently reported about the upbeat Miami condo market:

Infinity at Brickell 1 Bedroom – Lowest Price Per Square Foot Unit Available

We recently received a new listing at Infinity at Brickell that should capture the interest of anyone currently in the market for a 1 bedroom loft located in Brickell. Our listing is for a 1 bedroom/1.5 bath bi-level loft with 993 square feet of interior and a 76 square foot balcony off the living room. The asking price is $297,888, or $300 per square foot, making it the lowest price per square foot unit currently available for sale on the MLS or through the developer. The decorator-ready unit comes with stainless steel appliances, a stackable washer/dryer and one assigned parking space. The east-facing loft has a view of Biscayne Bay and the Brickell skyline from the 30th floor.

With less than 10 units remaining, developer inventory at Infinity at Brickell is on the brink of being completely sold out. The last remaining developer units are being offered considerably higher than $300 per square foot. This could be your last opportunity to own at Infinity at Brickell for less than $300 per square foot. If interested, feel free to contact us with any questions or to schedule an appointment to view the unit in person. You can reach us via email at [email protected] or by phone at 305-428-3860.

Miami Condo Prices Up 4 Months in a Row

A report released by the Miami Association of Realtors revealed that Miami condo prices have risen for the fourth month in a row. Since last November, the average sales price for condominiums increased 21.5% on a year-over-year basis from $193,486 to $226,151. The average sales price for single family homes in Miami also fared well with an 8.2% increase in the same time period from $300,369 to $324,846. Cash transactions accounted for 79% of all condominium closings and 41% for single family home closings.

Residential inventory in Miami-Dade County has dropped a whopping 40% over the past year with 14,461 active listings at the present time compared to 24,278 active listings a year ago. Foreign buyers are the main reason for the dramatic recovery Miami has experienced since 2008.

BrickellHouse Renderings

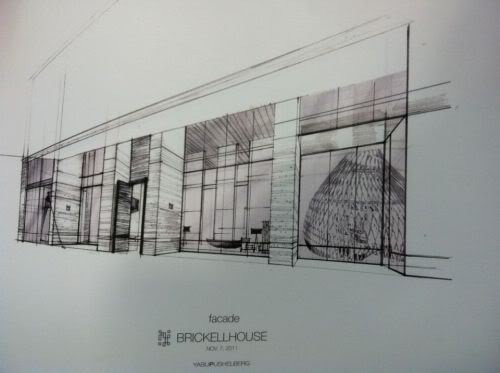

Up until now, interior renderings for BrickellHouse have not been made available. Earlier today, however, I was able to get my hands on a few initial designs created by the award-winning interior design firm Yabu Pushelberg. Yabu Pushelberg has designed the interiors for a number of exceptionally high quality condominium developments in South Florida which include Apogee South Beach, W South Beach and the soon-to-be-opened St. Regis Bal Harbour. That should give you an idea of what to expect from BrickellHouse when it is completed in 2014.

These are hot off the presses. As you can see these were dated November 7, 2011 and were released to the developer earlier today.

Miami Condo Glut is Coming to an End – reports The Wall Street Journal

In an article entitled “Miami Condos on Upswing,” The Wall Street Journal reported late Tuesday night that the Miami condo glut may soon be over as evidenced by recent sales activity. The article points to a 539-unit bulk deal at Midtown Miami which recently sold for $110M, or $183 per square foot. More importantly, the “acquisition represents one of the last remaining 100-plus unit bulk condominium opportunities in all of South Florida”.

The article also states that Icon Brickell, with 1,796 total units, now has fewer than 20 units remaining as of October and is expected to sell out in November. In my opinion, the sell-out of Icon Brickell will ultimately be heralded as the true end of the Miami condo glut. Icon Brickell was depicted, by the media and everyone alike, as the poster child of condominium over-development in Miami and, to me, is as symbolic as it gets. Once the last unit at Icon Brickell closes, those with real estate interests in Miami might as well bust out their vuvuzelas and make some noise because the biggest hurdle will have been overcome for the Miami real estate market.

The recent launch of sales at Paramount Bay is mentioned as well in the article. Paramount Bay launched sales around mid-October. I was recently told that 70 units at Paramount Bay have now either closed or are under contract. More surprising, is the fact that only 4 of the 11 total penthouses remain. None of the penthouses at Paramount Bay with the large terraces (1945 square feet to 2949 square feet) remain available. Given that terraces of that size are rather unique in Miami, there was a mad rush by buyers to grab those. Prices for penthouses at Paramount Bay with the large terraces were priced around $2.1M to $2.9M – a good indication that the luxury market in Miami is also performing stupendously.

Marquis Residences, a 292-unit luxury condo development located in Downtown Miami which was not mentioned in The Wall Street Journal article, hit an important sales milestone recently. I was informed last week that Marquis Residences is now over 75% sold. Remaining 2 bedroom condos start at $590,000 while remaining 3 bedroom condos start at $860,900. A few penthouse condos at Marquis Residences also remain available for sale.

Vizcayne, another condo development in Downtown Miami with remaining inventory, is now over 50% sold. Earlier this week, it was announced that no-doc seller financing is now available with 30% down to qualified buyers. That should make Vizcayne a very popular option among investors once this news is disseminated. Vizcayne prices range from $200K to $2M.

Inventory of new construction condos in Miami continues to dwindle with each successive month. By all accounts, it very well seems that 2011 will go down as the year that the Miami condo glut came to an end. With the worst behind us, I see 2012 filled with announcements of additional pre-construction condo developments throughout Miami. It will be the year that construction cranes will once again grace our skyline to fulfill the future demand for condos in Miami.

MyBrickell Sales Officially Launch; Prices Start at $177,900

Last night’s gala introducing Karim Rashid, the world-acclaimed interior designer behind MyBrickell, marked the official launch of sales for the condo development. MyBrickell is off to a tremendous start with over one-third of the condos already reserved. That is quite an amazing feat given the fact that reservations were not being accepted until just 11 days ago. The level of success that MyBrickell has experienced thus far helps to understand the level of demand that still remains for new condo inventory in Miami.

MyBrickell will have a mix of studio, one bedroom + den, 2 bedroom and 2 bedroom + den units. Prices start at $177,900 which is excellent, in my opinion, given the current availability of Brickell condos in that price range. To put the pricing for studios into perspective, there are currently only 4 studios in Brickell priced under $200,000 for sale on the MLS. Two of those studio condos are located at The Four Ambassadors (built in 1968), one at Brickell Townhouse (built in 1963) and one at Brickell Bay Tower (built in 1964). Furthermore, two of the four listings are short sales. It goes without saying that MyBrickell will be a brand-spanking new condo development when it is completed and delivered in 2013 to those with reservations. I may not have a crystal ball, and cannot tell you with certainty where prices are headed, but I can pretty much guarantee you that there will be less condo inventory in Brickell in 2013 than there is now. Moreover, MyBrickell will be the only Brickell condo development to hit the market that year.

One of our clients attended the MyBrickell sales event last night and reserved a 1 bedroom + den. Her price – only $228,000! With pricing like that, it helps explain the rush by people to reserve condos at MyBrickell.

Below, you will find the price ranges for condos available at MyBrickell. The average price per square foot for MyBrickell hovers around $300.

Now that sales have officially launched at MyBrickell, you are able to receive pricing for specific units and reserve one immediately if you choose to move forward. Please refer to our MyBrickell profile page with renderings, building and unit information and pricing. There, you may also download the MyBrickell e-brochure as well as the reservation agreement and wire instructions. Feel free to contact us if you have any questions or an interest in reserving a condo at MyBrickell.

BrickellHouse Floor Plans, Info and Pricing

BrickellHouse is now accepting reservations. The 374-unit condo development will be located directly west of Jade and north of Emerald at Brickell at 1300 Brickell Bay Drive. BrickellHouse has several appealing features but there are two which will also make it rather unique. One, it will allow daily rentals but will not be considered a condo-hotel. The building will have on-site maintenance and housekeeping staffs as well as an in-house management program for owners who wish to rent their units on a daily, weekly or monthly basis. Owners will obviously first need to finish and furnish their decorator-ready unit in order to be included in the leasing program. You can read more about this program in the BrickellHouse brochure. The second unique aspect of BrickellHouse is the parking. The building will have a fully-automated parking garage.

The 46-story high-rise will have an array of lavish amenities which include:

- rooftop pool and sundeck

- fully equipped, state-of-the-art fitness center

- luxury health spa with sauna, steam and private treatment rooms

- High-definition theater room with 10-foot screen and theater-style seating

- Private owner’s lounge with event bar, catering kitchen and daily world newspapers

- Resort deck with putting green and summer kitchen

- 50-foot-long lap pool with poolside cabanas and heated Whirlpool spa

- Resident club room with conference and meeting rooms

- 24-hour concierge and security

- 24-hour guest valet parking

Additionally, Meat Market, a steakhouse on Lincoln Road in South Beach, has already signed on to occupy part of the retail space on the ground level of BrickellHouse.

BrickellHouse will be comprised of studio, 1 bedroom/1 bath, 2 bedroom/2 bath and 3 bedroom/3 bath units. The spreadsheet below will show you the approximate interior and exterior square footage for each. You can also refer to the BrickellHouse floor plans where you will also be able to view layouts for the BrickellHouse penthouses.

A full price list has not been released but the pricing below will give you a general idea for what one might be able to afford at BrickellHouse. Contact us if you have an interest in purchasing a unit at BrickellHouse and we will be able to get you pricing for other units.

Studios

- Unit 2212 (S3) – $163,900 west view

- Unit 1906 (S1) – $197,900 eat view – (420 sq ft under a/c)

1 bed/1 bath

- Unit 2507 (A7) – $276,400 east view

- Unit 2511 (A5) – $273,900 west view (790 sq ft under a/c)

2 bed/2 bath

- Unit 2507 (B4) – $435,900 east view

- Unit 2002 (B5) – $331,900 west view (1,116 sq ft under a/c)

2 bed + den/2 bath

- Unit 3008 (B1) – $424,900

3 bed/3 bath

- Unit 3002 (C1) – $683,900 (1,451 sq ft under a/c)

Contact us at 305-428-3860 or [email protected] to learn more about BrickellHouse.