Terra’s David Martin Debuts his New Real Estate Column in Forbes

David Martin

A warrior and a poet? Meh. Maybe not, but David Martin, head of Terra Group and developer of Grove at Grand Bay, Park Grove, and GLASS, is now a developer and an author. He’s writing a twice-monthly column over at Forbes on ‘real estate development, design, and sustainability,’ beginning with a discussion on why more buyers in South Florida are end users these days as opposed to speculators. To summarize his point in just a few words: Miami’s a bit more grown up, and that makes a big difference.

Centro Moves Closings & Gets Fannie Mae; Check Out Our Drone-Cam!

Centro. Photo by Lucas Lechuga.

Just like everything from Miami’s biggest construction projects to your Memorial Day flight, closings at Centro have been slightly delayed. A month ago we heard word that the project was wrapping up construction and aiming to acquire their TCO by the end of May/beginning of June, allowing residents to close on their units and move-on-in. Now, according to representatives of the project, they’re talking more like the end of June. Okay, so not a big shocker. Stuff happens. Centro, in the heart of Downtown Miami, is still rapidly progressing toward completion.

If you’re the kind of bloke who likes his condos finished before he buys one, Centro does have some units left, with 645-foot one bedrooms starting at $303K, up to 1131 square foot 2 bedroom/bath units topping out at $578,900. Finally, if you’re the kind of bloke who needs financing and you really want to live at Centro, well you’re in luck too. Centro was granted conditional approval from Fannie Mae (warning: PDF) at the end of last month, lasting through January of next year.

And if you’re wondering the type of views that Centro will offer, look no further. Check out the cool drone video below which showcases the building and fabulous views that it offers.

New Video Released for Paramount Miami Worldcenter Showcasing the High Street Retail

A new video was released today for Paramount Miami Worldcenter and includes footage of what the high street retail will look like once finished. Well, the video isn’t exactly new. It’s an edited video with all references of the mall removed and, in its place, new footage showcasing the high street retail. Spoiler alert: It looks amazing!

Almost Sold Out, Two Park Grove Begins Concrete Pour at 2 AM Tonight

The tower in the middle is Two Park Grove.

Up late and in the mood for a show? The foundation pour for Two Park Grove, starchitect Rem Koolhaas/OMA‘s first residential tower in the United States, is beginning at 2 AM tonight and will continue until 4 PM tomorrow. The first of the three Park Grove towers to begin construction (so… Rem Koolhaas’ first, second, and third residential towers in the U.S.) Two Park Grove is being co-developed by the Related Group and Terra Group, and is about 97% sold out (with pricing starting at $2 million). According to the press release 2,600 cubic yards of concrete will “lay the foundation for an elevated 3-foot deep concrete slab at its core that will support the faceted tower columns…This pour requires four pumps and the labor of over 100 people placing up to 400cy/hour.”

One River Point Rendering Crush

Typical Unit Interior

One River Point, the ultra-luxury residential and hotel project planned for the Miami River that has Hong Kong-level service and a boat valet, just released new renderings of unit interiors, showing off mighty deal balconies, vast great rooms, and views that seductively mix water and city. Other renderings, most of which are older but just as sexy, show the project’s twin towers connected by a gigantic bridge and private club floating in the sky, a huge waterfall, the main pool, and the exterior from various angles. Designed by starchitect Rafael Viñoly and developed by KAR Properties, One River Point is taking reservations at the moment. It’s also the fanciest place to hit the Miami River probably ever.

On the River the Old Epic Sales Center is Being Demolished, While Met Square Construction Continues

Former Epic Sales Center. Photo by Lucas Lechuga.

An Argentine developer and grocery store mogul has finally begun demolition of the former Epic sales center at 300 Biscayne Boulevard Way, on the Miami River. The Next Miami has some closer photos of the demolition. The over-the-top 2.5 story structure has stood there far beyond its planned lifespan, more recently acting informally as sort of a yacht club for the superyachts tied along its river dock. (we don’t know how much of the interior was utilized for this secondary purpose, but the parking below the elevated structure was) Epic developer Ugo Colombo sold the 1.25 acre wedge of land for a whopping $125 million to German and Gloria Coto, whose family is best known in Argentina for their supermarket chain. The Cotos are planning an 817 foot ‘lighthouse’ condominium tower on the site.

Meanwhile, across the street construction continues at Met Square, the last element of the Metropolitan Miami megaproject which has been years in coming.

Met Square construction. Photo by Lucas Lechuga.

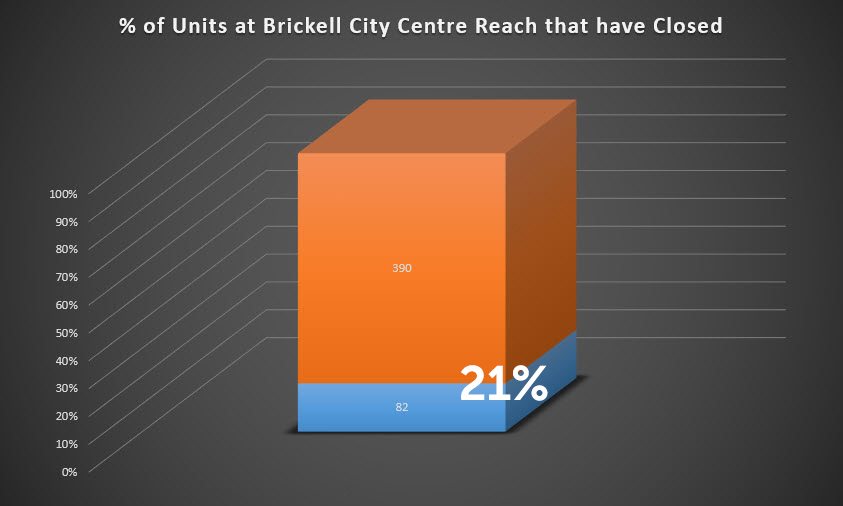

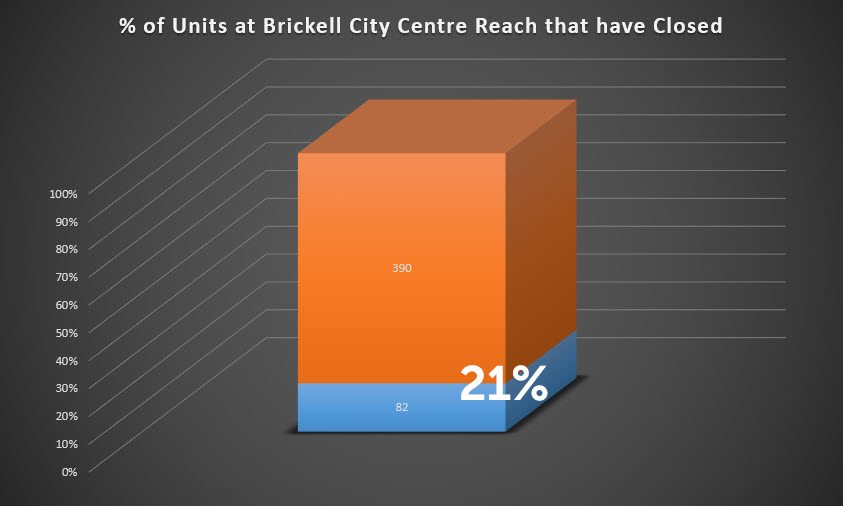

Closings at Brickell City Centre Reach Tower: How are They Faring and What Percentage are Hitting the Market For Rent?

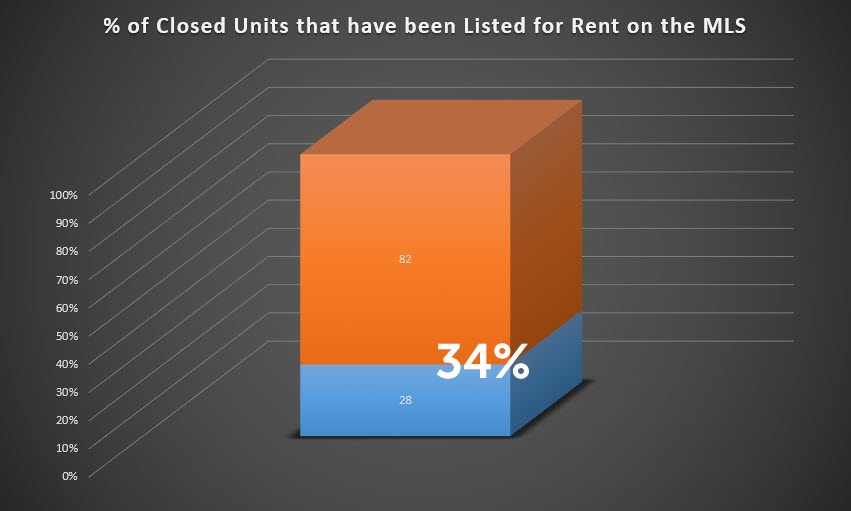

According to public records, closings for condos in the Reach tower at Brickell City Centre began on April 11, 2016. Since then, as of this past Friday, 82 of its 390 total units (21 percent) have been recorded as closed. The 82 closed units amount to $64M in closed sales, averaging $619 per square foot, and ranging from $532 to $674 per square foot. Of greater significance, to many at least, is not the percentage of units that have closed, but, rather, the percentage of closed units that are being converted to rentals. In other words, what percentage of the units at Brickell City Centre were purchased by investors versus end-users? That’s a question that has crossed my mind a number of times in recent months, so I decided to do some investigative research. According to the MLS, 28 of the 82 recorded closed units (34 percent) have already been listed for rent (25 units available for rent + 3 units pending). If that percentage ends up holding true across both towers at Brickell City Centre (Reach and Rise), that will mean that roughly 265 units will end up hitting the market for rent soon after closing. However, it should be noted that Swire (the developer) appears to be closing lower floor units first. Of the 82 closed units, the majority of them are located below the 20th floor; the highest floor that a closed unit is located is the 30th. The Reach tower at Brickell City Centre is 43 stories high, as is the Rise tower. In my experience, investors tend to snatch up the lower floor units because they tend to bring the highest rate of return from an investment standpoint. As such, if we were to divide the tower in half, I would expect the bottom half to have more units owned by investors than the top half. With that being said, I do not expect the 34 percent rental-to-closing rate to hold true as closings continue. If I were to venture a guess, I would say that the rental-to-closing rate across both towers will end up being closer to 28 percent once everything is said and done. But we shall see, because I plan to report each month an update on closings, not only for Brickell City Reach and Rise, but for all recently completed condo developments. Back in 2007, 2008, and 2009 (during the last condo boom), I reported closings rates a lot. Consider this a reboot.

Tennis Pro Andy Murray Unloads Condo at Jade Brickell

Andy Murray’s Condo at Jade Brickell.

Tennis pro Andy Murray, currently ranked the #2 tennis player in the world and a 2012 Olympic gold medalist, is selling his $2.9 million 45th floor unit at Jade at Brickell Bay, according to Variety’s Real Estalker. The Scotsman picked up the unit, with distant views of the tennis center at Crandon Park, in July 2008 for $1.575 million, must have used Jade Brickell Unit #4501 as a vacation home since then (as evidenced by the limited interior decoration and kitschy Union Jack pillow as a memory of home), finally listing it for $2.9 million. MLS data now indicates a sale is pending.

Since setting up camp at Jade, Murray picked up two UK homes, including a ‘mock-Regency’ outside London, and a 19th century Victorian mansion called Cromlix house outside his hometown of Dublane. Just like many a local boy gone big, yes even Murray returned home to nab the village manor. Museum or not, just think of how many a very young Miamian has walked into Vizcaya and thought “someday I’ll buy this place.” No word yet on whether Murray is finding somewhere else to stick his flagpole in Miami, or going home to play ‘country squire’ full time.

Photo courtesy Miami MLS

Did a Kaleidoscope Explode in This Modernist Condo?

Santa Maria condominiums, one of Brickell’s most stalwart high-end condo towers, is where you would be likely to find somewhat predictable interior design choices, liked overstuffed club chairs and wainscoting set off by a Dale Chihuly chandelier. Unit 1643, priced at $5.5 million, has none of those things. Instead it’s a white box condo with bold, solid colors, and geometric designs selectively streaked over walls, ceilings, and floors. The dining room comes in a black & white diamond pattern. There are yellow checkerboard-ish walls in a bathroom. The kids’ rooms are colorful, as kids’ rooms tend to be, and the kitchen is triangular. Out in the living room, a giant circular black rug and three-piece yellow couch dominate the space, while on the balcony the ottomans are made of grass.