People often ask me why I chose to focus on condominiums rather than single family homes when I began my career in real estate. I guess the answer is mainly attributable to my formal education and the work experience I gained after graduating college.

As mentioned in the About Me section of this site, I graduated from the University of Illinois at Champaign-Urbana with a Bachelor of Science Degree in Finance with a specialization in Investments. After graduation, I worked as an equity options trader on the floor of the Chicago Board of Options Exchange for four years.

It became second nature for me to begin to analogize most aspects of my life in investment terms. Condominiums to me had similar homogeneous characteristics as that of a financial security than single family homes.

In my opinion, it is much easier to analyze the true market value of a condominium than it is for a single family home. A price per square foot analysis of condo units in a building, and even a neighborhood, reveals more truth than the price per square foot analysis of single family homes on a particular street or in a particular neighborhood.

A 2 bedroom condo in a particular building, in many instances, will have the same characteristics of another 2 bedroom condo in that same building, such as shared common areas, amenities, year built, square footage, appliances, floor plan, maintenance fees, view, parking spaces and so on. Any differentiations in the aforementioned qualities can be easily adjusted in the value of the subject property versus comparable properties.

It is much more difficult to assess the value of a single family home. It is common to see a small, outdated home situated right down the street from a large, recently built home. Of course there are ways to appraise the values of each by making adjustments for any differentiations in each home but it just isn’t the same, in my mind. A home buyer may fall in love with one home while he or she finds the home right down the street an eyesore.

It becomes much more expensive to turn a home down the street into your dream home than it is to turn a condo down the hallway into your ideal abode. The expense of replacing or changing the floors, paint job, window treatments, light fixtures and other elements of a condo can more easily be ascertained.

These thoughts guided me into the decision of choosing to specialize in condominiums over single family homes when I began my career in real estate. As the housing bubble talk began to escalate a few years ago, I began to think of how nice it would be conceive a way to hedge real estate investments for the average home purchaser or investor in case of a bubble-popping scenario.

I guess fellow Chicagoans at the Chicago Mercantile Exchange had similar thoughts. They created a tradable home market index based upon the Case-Shiller Home Price Index, which measures home prices based on recorded changes in home values and a repeat sales methodology.

The futures and options instruments that were enacted by the CME began trading in May of 2006. The purpose was to offer jittery homeowners a way to hedge the investment in their homes against future price declines. The CME also saw a large interest from investors to directly participate in the much-talked-about housing market.

While being a giant leap in the right direction, the CME’s housing index is far from perfect. They introduced tradable securities based upon large metropolitan areas which include the following: Miami, Chicago, Boston, Las Vegas, Los Angeles, New York, San Diego, San Francisco, Denver, Washington, as well as a weighted composite index.

However, it is difficult to adequately hedge the value of a condo in a building such as The Setai in South Beach from a condo in a boutique building in Hialeah using their index.

I have decided to create my own, localized, index. This index will be based upon market data derived from major condo buildings in Miami. I will create a graphical representation of a six-month price per square foot moving average using data of closed sales and a month-to-month price per square foot analysis of units currently on the market. I may include other relevant statistics in the future to provide more in-depth information relevant to the Miami condo market. I hope you guys trading the Miami housing index at the CME appreciate the information. I’d love to hear from you.

I plan to release an index update each week. At the outset, I will rotate Miami neighborhoods for a total of four neighborhoods (South Beach, Brickell, Arts & Design District and Miami Beach minus South Beach). In the future I plan to add Downtown Miami and Park West as its own index once the nearly constructed buildings in those areas are fully built.

I’ve decided to name my index the “Miami Condo Index”, or MCI for short. Obviously my index won’t be tradable as is the Chicago Mercantile Exchange’s housing index, but I hope that it will provide more insight to localized housing markets throughout Miami’s major neighborhoods.

The Miami Condo Index will launch next week with an in-depth look at Brickell.

I urge other Realtors throughout the country to create their own localized housing indices to fully encompass their own markets and provide market transparency to home buyers like no other.

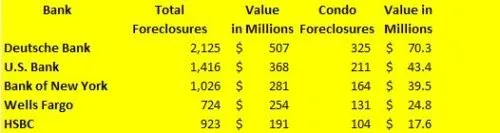

Deutsche Bank Leading the Way in South Florida Foreclosures

Daily Business Review published a very interesting article today entitled “Special Report: Condo Lending”. It provides a list of the top five banks who have filed the most foreclosure actions from January 1, 2007 to May 4, 2007 in South Florida. Below is that list:

The most revealing part is that these banks have no reason to be overly concerned. In most cases, the loans were repackaged as mortgage-backed securities and sold to Wall Street investors. Public records may reveal the banks as the possessor of these loans, because their names are still associated with the notes, but it is the investors who will bear the monetary loss due to the risky underwriting practices of these banks. In fact, the banks actually make additional money by charging fees to the investors by acting as custodians in managing the foreclosure proceedings for them. Helluva a gig! They’re making money on the front-end and back-end!

Mortgage Rates Continue to Head North

Existing home inventories are up, foreclosure rates are rising and mortgage rates continue their ascent – talk about bad medicine for the current lackluster real estate market! CNN.com reports that 30-year fixed rates have jumped to 6.53%, their highest level in 10 months. While rates, a year ago, were slightly less than they are now, the state of the real estate market was in much better condition 12 months ago. An increase in rates now only amplifies the problems that exist.

The Mortgage Bankers Association (MBA) expects 30-year rates to hit 7 percent by year’s end. The Mortgage Bankers Association (MBA) and the National Association of Realtor don’t foresee a recovery until the beginning of 2008. This foreseen recovery has been pushed back a number of times, and at one point early this year a slight increase in home prices for 2007 was predicted. In real estate markets, such as Miami, I expect this recovery timetable to continue to be pushed back until early 2009. The number of new units coming to market actually increases next year and doesn’t drop off until the following year. There’s no denying that the South Florida real estate market is a safe long-term bet as it will become one of the top retirement destinations for the millions of Baby Boomers set to retire in the next ten years, but demand has to catch up with supply. That will take some time.

Those people holding preconstruction contracts will soon seek financing to close on their condo units. For those that are questioning whether to walk away from their deposit or to close on their condo unit, the ever increasing rates will make their decision a little easier.

The Wall Street Journal: Florida Hones Plan to Overhaul Property Taxes

Yesterday, The Wall Street Journal published an article that most of you will find interesting. The article is entitled “Florida Hones Plan to Overhaul Property Taxes”. It discusses a proposed property-tax relief plan that could provide a second wave of buying throughout Florida. There are a number of homeowners in Florida who would like to upgrade to a newer home but are unable to because their property tax bill would skyrocket. For example, Miami Democrat Dan Gelber, who is mentioned in the article, says that his property taxes would go from $7,000 per year to more than $20,000 per year just by moving across the street to a similar home. Several state governments in the United States are working to provide property-tax relief to homeowners but Florida’s proposed property-tax relief plan will by far provide the greatest benefit. The plan could provide over $30 billion worth in property-tax relief to homeowners over the next five years.

In talking with clients in the last couple of months, it seems that most are awaiting word from the state legislature to see what they decide. The last two weeks real estate activity has been quiet as everyone waits for the state legislature to convene in mid-June. There is no doubt that this could be the catalyst needed to reinvigorate the current stagnate real estate market throughout Florida. Let’s keep our fingers crossed. I will provide further updates on this topic as new developments become available.

Securing a Loan Gets Tougher

The Wall Street Journal, this past week, published an article entitled “Securing a Loan Gets Tougher as Lenders Tighten Standards”. The opening two paragraphs are as follows:

Mortgage lenders are beginning to scrutinize borrowers more closely, causing some loan applicants, even those with good credit, to face higher costs and more hassles.

As the number of delinquent mortgages climbs, lenders have tightened their standards for issuing loans, including such well-publicized moves as raising minimum credit scores and cutting back on 100% financing and low-documentation loans. Now, some lenders are probing more intently would-be borrowers’ finances. They are taking a tougher look at how much the property a borrower wants to buy is worth. They are peering further into clients’ pasts for credit problems and requiring more in-depth reviews of borrowers who say they are self-employed. Some lenders are taking a harder stance when it comes to whose credit score a couple can use when applying for a mortgage, rather than simply allowing them to use the higher of the two scores.

A few days ago, I had a conversation, via email, on this very topic with a friend of mine who is a mortgage broker in Miami. One of my earlier blogs entitled “Vue at Brickell – Overpriced or Insanely Overpriced?” was what initiated this conversation. A few of his comments are below:

So you know, most lenders will not do anymore loans in Brickell, especially on investor stuff. All of the new buildings will have problems in the next few years. There was just so much fraud there.

My Opinion: 99% of lenders these days will only lend on the last MLS price, not the appraisal like they did in these cases. Also in Brickell they will do appraisal reviews and BPO’s to be sure on any borrower with less than stellar credit and a 20% down-payment. The cash back deals are still occurring, and the fraud line is getting blurred. So you know the current state of things, if the borrower is being approved by the lender on the MLS price, and they are not falsifying any of the loan criteria that makes them “approved” by the lender for the transaction then there is no fraud. Even if the seller decides to give some cash back to the borrower -typically structured to a third party company (aka the borrower), this is technically not illegal, because the cash back did not affect the underwriters decisions and the borrower was truly qualified and the price was justified by the MLS (market) and the appraisal. So what is occurring is sellers are giving cash to the borrower after the sale, which legally they are allowed to do. Gray area of the law -Yes, and this is occurring rampantly today. There are hundreds of investor buyers – maybe they learn from some info-mercial somewhere about this – I don’t know- but I am called every month from new clients with these “legal” deals. In my opinion the Developers are in the fray on this type of deal with leasebacks, mortgages ad to pay your bills for up to 2 years and cash back at closings this “legal” way. What you will find is this type of thing is “propping up” the market in the short term and creating false market conditions due to buyers paying more in expectation of a large cash back to financially carry the property – or receiving their “profits” on the front end and leaving town or the country. My forecast, is that the lenders will begin to audit buyers and especially the 1 payment default foreclosures for this type of dealing and press the state of Florida to amend laws and prevent this type of dealing. Today its a loophole, I foresee in a year after the scams take their toll, this will also be an issue in the news and another result in excessive foreclosures.

This is very bad news for investors who bought preconstruction condominiums in some of these buildings that are due for completion in the next two years. Many have feared that a large percentage of these investors will be unable to close on their condo units due to the financial burden of having an extra mortgage. Now, if banks are unwilling to underwrite investment loans, there becomes a fear that people will be unable to close because financing will be unobtainable. People will have no choice but to walk away from their deposits, which in most cases amounts to 10%-20% of the purchase price. Developers will have no choice but to offer significant incentives or slash their prices on the remaining condo units in their inventory that were unable to close. Either action will likely bring down prices in surrounding buildings and have a negative impact on the entire real estate market of that neighborhood.

Vue at Brickell – Overpriced or Insanely Overpriced?

I’d have to go with the latter on this one. A look at the current inventory of condo units for sale at the Vue at Brickell will show that the average price per square foot that these units are currently listed for is over $550. $550 per square foot! That’s for a non-waterfront condo unit, with partial bay views at best, in a building that is, by most standards, NOT a luxury high-rise building. In fact, Vue at Brickell was formerly known as Summit Brickell View when it was a rental building. The acquisition of the Summit Brickell View was made in December 2004 and conversion of the 323 units to condos began quickly thereafter. Grant it, the Summit Brickell View had recently been completed when the acquisition was made, and almost 70% of the units had never been occupied. Either way, it had, and in most cases still has, the features of a rental building. The majority of the units currently for sale still have the ceramic tile and carpeting throughout just the way they were sold when the units were sold as condos. The pictures below will show you a typical unit at Vue at Brickell.

Keep in mind that this is a typical unit at Vue at Brickell. I realize that some units have upgraded flooring and appliances, but the majority of units listed at Vue at Brickell look like this. Some units are even listed at over $700 per square foot! Those better come with marble floors, a Sub-Zero refrigerator, a Miele dishwasher, and a butler and maid! But they don’t even come close. In fact, two of those listings priced at over $700 per square foot come with ceramic tile and carpeting throughout, just as they were when the building was known as Summit Brickell View. One of those listings says “motivated sellers”. Motivated? Maybe they’re motivated to WAIT. Even the three bank-owned listings in this building are overpriced, ranging from $436 to $510 per square foot.

So what made this building so insanely overpriced? Did everyone get together and smoke the wacky tobacky without me or is something more afoul going on here? A look at closed sales for 2007 in the building reveal that mortgage fraud may have been the culprit. Three of the eight closed sales in 2007 sold for prices much higher than the asking price. Here they are below:

List price: $549,995

Sales price: $720,000

List price: $619,000

Sales price: $770,000

List price: $647,000

Sales price: $830,000

These types of cash-back deals have been the focus of a recent mortgage fraud investigation throughout the country. A cash-back scam occurs when a buyer offers to pay a significant amount more than the asking price, with the difference returned to them at closing. Most banks like to keep the cash-back amount to no more than 3% of the purchase price, and almost all lenders have a ceiling of 6%. In most cases, the seller and the listing agent are not aware that anything wrong is occuring and are just happy to have finally sold the property. Lenders, on the otherhand, are unaware of these large cash-back payments because the details of the arrangement are concealed within an addendum that does not get submitted to the bank along with the rest of the sales contract. Unscrupulous appraisers are often used to justify the inflated value of the property and the bank lends based on the purchase price stated on the contract after review of the appraisal.

It is no secret that Florida is well known for the mortgage fraud that has been running rampant throughout the state. In fact, according to a report released by the Mortgage Bankers Association, Florida led the nation in mortgage fraud in 2006. Hopefully, the mortgage fraud investigation throughout the state, and the rest of the country, will put an end to this nonsense so property values can return to an equilibrium state as dictated by the law of supply and demand.

If my assumptions are correct, and previous condo owners at the Vue at Brickell did fall prey to this sort of cash-back scam, then prices there will come in for a crash landing. There’s another building in Brickell that I feel may have a similar fate but I’ll leave that for an upcoming blog entry.

Subprime Mortgage Fallout

An article posted today on CNN.com, entitled “Speed of subprime bust surprises lenders”, discusses how the speed and depth of the subprime mortgage fallout has surprised even those who had predicted its occurrence. Banks have stopped offering a variety of mortgage loan products that were prevalently available last year. There is no doubt that the subprime mortgage collapse has put a halt to the once red-hot real estate market and has pushed home prices lower as people across the country face foreclosure. Many would argue that these risky loans acted as the fuel that drove home prices far higher than expected.

Banks, looking to stay afloat, have become much more flexible in negotiating outstanding mortgage debt in hopes to recover a good portion of their loans rather than being at the mercy of the foreclosure and auction processes. Foreclosure inventories, and that of existing homes for sale, has gone up considerably this year. Coupled with the large number of housing units coming to market throughout the country in the next 12-24 months, the real estate market may be in far worse condition than many had expected.