IconBrickell Pool Closure Begins December 5

Over a year after we first reported the pool closure at IconBrickell, they have finally given the dates for the work to begin. In a letter to residents this week, the condo association has announced that starting December 5, the pool will be inaccessible for approximately 12 months. Surprisingly, the condo association did not make arrangements for an alternative pool for the residents.

Anticipation of the repair and special assessment have sent sale and rental prices in a tailspin. Sales prices in the last 90 days are averaging $426/square foot. Just a year ago, apartments in the project were closing at $584/square foot.

Rental prices have also been in free-fall. Unit 4103 in Tower 2 rented in 2015 for $5,300. This year, it rented for $3,800 after 5 months on the market. In Tower 1, unit 4104 rented this month for $2,000, down from the $2,600 that the landlord received last year. It doesn’t help matters that there are currently 180 available rentals on the market. Since 24 apartments rented in the last 30 days, it will take over 7 months to absorb all of this inventory.

On the bright side, this is a fantastic opportunity for investors who are looking for a long-term hold or for those who are looking for a great price on a vacation home. While the values are depressed now, I fully expect them to rebound when the amenity deck reopens. There are still plenty of sellers who need to move on from the properties for personal reasons, or investors who are not able to wait out the storm. How much lower do you anticipate the prices will fall? We are happy to help if this situation is an opportunity for your investment goals.

Tenant Sues Condo Association For Price Gouging On Application Fees

Quantum on the Bay

A tenant at Quantum on the Bay in the Omni district finally did something about the high application fees that are being charged to prospective tenants, according to the Miami Herald. He is suing them because their application fees are in excess of the $100 cap that the Florida statute issues.

This has been an ongoing problem for tenants in many of the Downtown area buildings for several years. Some condo associations use these elevated fees in order to avoid having to make a special assessment on the unit owners for repairs or upgrades. The association at Quantum once had a $400 application fee, but it was later reduced to $150 after so many potential tenants complained. In order to continue bringing the income that they once received from the application fees, they split it into the application fee plus the administrative fees. Some other buildings have ‘impact fees’ of $500, but Quantum is one of the highest priced buildings in the area for a tenant to apply for.

Even though it is not lawful for a building to charge these exorbitant fees to tenants, many still do. The tenants really have no choice but to accept the fees. Protesting only causes delay and added expenses. If they miss their move-in date, they would need to stay at a hotel until the issue is resolved and there is still no guarantee that it would be resolved in their favor without a lawsuit. The Government Affairs department of our Miami Association of Realtors has been lobbying in Tallahassee for some time already, trying to convince them to enforce the laws.

Now, most buildings also charge a security deposit for the common areas and for pets, but that is different. Security deposits are returned. We typically see a security deposit that is held through the duration of the lease in order to guarantee there will not be damage to the common areas, a smaller security deposit for the actual move to guarantee that the elevators and hallways are not damaged by the movers and/or a pet deposit to the building.

You can read more about the Florida Condominium Act here, so that you know your rights. While it seems that Quantum is being singled out, this is a large problem throughout the marketplace and something that we are striving to change. On a day to day basis, the best we can do is see that our clients get settled as peacefully and efficiently as possible. On a larger scale, we are very much a part of the efforts from the Miami Association of Realtors to bring change to this practice.

FHA Proposes New Approval Process That Helps People Get Condo Loans

Condo shoppers rejoice! The FHA (Federal Housing Administration) is proposing changes to their condo approval process that could really benefit South Florida shoppers.

Up until now, if a person wanted to buy a condo in the Downtown Miami, Brickell, Midtown, or Miami Beach areas with an FHA loan, their choices would be to buy at Brickell on the River’s south tower, Brickell on the River’s south tower, or Brickell on the River’s south tower. That is not a typo, the only approved condo project in our area is Brickell on the River. The entire project isn’t even approved, just the south tower. 1800 Club was approved in 2012, but that expired in 2014 and wasn’t renewed. In my experience, whenever I have a buyer who is looking to use an FHA loan, I always tell them that they need to purchase a house, not a condo. Condo FHA loans are almost impossible.

The problem is that in order to offer FHA loans on the properties in the various condos, the entire building has to undergo an application process with FHA. This isn’t cost effective for developers because they have typically already sold their units prior to the building’s opening. Established condos would have to undergo the expense of the application, which is another expense for the condo association to pay. Those buildings that do go for the application typically get rejected because of the number of owner-occupants in the building. Let’s face it, a lot of the residents in our towers are vacation homes, rental units, or a combination of the two.

Well today is a new day. The FHA has realized that it is extremely difficult to use their loans in condos and are proposing to change their ways. They are proposing to lower the minimum owner-occupancy requirements to 25%-75% and allow single-unit spot approvals.

What this means is that instead of having to qualify the entire building, you could get an FHA loan on a single condo as long as their building information matches the requirements of FHA (which would now be far more lenient). Since FHA loans are designed for people who are responsible homebuyers but may not have a huge down payment or fully-established credit, these buyers have been left out of the Downtown Miami market, which is in need of new buyers now. Let’s hope and pray that this goes through! It would be amazing to see more homeowners in the downtown area!

If you would like to read the entire proposed rule, you can find it here.

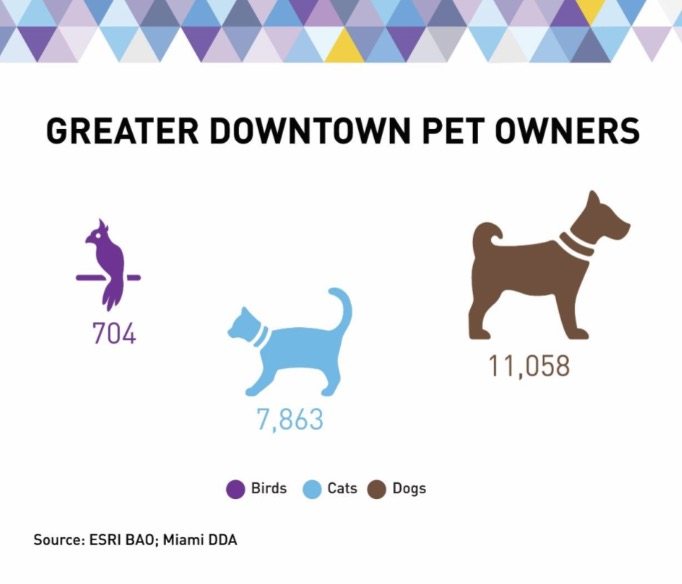

Almost 40% of Downtown Miami Residents Have Pets – Strategies for Investors and Tenants

The Downtown Miami DDA (Downtown Development Authority) released its updated demographics study today, and they found that 39% of Downtown Miami households include a pet. This is interesting because so many of the developments impose strict pet policies upon their residents. Some only allow certain sizes of pets, some only cats, some only allow pets for unit owners and some say no pets at all.

This is always a touchy subject when we are working with a client who has a pet. There is so much misinformation out there regarding which buildings do and do not welcome pets. If a resident gets caught with an unauthorized pet, they are forced with the difficult choice of paying a lease cancellation fee (which is typically the value of 2 months’ rent), or re-homing their beloved pet. Unfortunately, not all agents verify the pet policies before entering into a contract, which wastes time and gets the client all excited about an apartment that they cannot have. No bueno.

I even once had a client who cheated on me with another agent that had told them they could have a large pet in a pet-restricted building. That is completely irresponsible and self-serving of that agent. Thank goodness, the clients realized what would happen if they went forward with that deal. The agent would have been paid and then they would have either had to break their lease or part with their dog. That is a horrible choice to have to make when most people consider their pets as members of the family.

In order to have an authorized pet in the building, many associations require an additional registration and application. The pet’s weight is verified (many times with a report from the veterinarian), their vaccinations are verified and some buildings even take it a step further. Infinity at Brickell requires a DNA sample to be placed on file and in the event that messes are found in the lobby, the mess is sent in for a DNA match. The resident that pops up after the DNA test is issued a fine. I call it Maury Povich enforcement… but it works. If people know they’re going to get busted breaking the rules, they’ll be less likely to do so. This way, the building can continue to allow large pets for everyone.

Over recent years, a popular workaround to the ‘No Pets’ buildings has become all the rage. There are websites where you can claim that you need a therapy dog. They’ll issue you a certificate for a fee and, viola! Your dog can go with you everywhere and nobody can say anything… except the condo associations have started to get wise of this ruse. The Jade at Brickell verifies these Therapy Dog certificates through an attorney. It takes an extra few days during the application process and you don’t get your application fees back if you get caught with a phony form. I don’t recommend the fake therapy dog stunt.

If you are curious of whether a particular building accepts pets, just have a look at the building page on our website. We have verified all of the buildings’ policies and list them in the FAQ section of the website. Every now and again, a building will change their policy in between when we last called to verify, but we update it frequently. Our agents also keep themselves updated of the pet policies and fees for the buildings in the area. We’re all about efficiency and not wasting your time or energy…

So what about investors?

With the rental market changing, it is important to have apartments that appeal to as many people as possible. Purchasing an investment condo for sale in a pet-restricted building automatically crosses out almost 40% of the prospective tenants that could be interested in moving in. Some of my favorite pet-friendly buildings are Marina Blue and 900 Biscayne Bay in Park West, Infinity at Brickell in Brickell, the Midtown developments in Midtown and One Miami in Downtown.

For investors who are concerned with having animals in your property without knowing the behavior or cleanliness of the pets, it is completely customary to charge a pet deposit for the unit. In many cases, the building has a separate pet deposit or fee, but I suggest a refundable deposit for the unit itself. The amount can vary depending upon the pet. Puppies would require a bit of a larger deposit since they tend to chew and have accidents. You could also lower the deposits in the event that a tenant was able to submit a diploma from obedience school or behavior training.

Whether you are an investor, or if you are buying/renting a home for yourself, if there is a specific building that you are curious about, don’t hesitate to drop us a line and inquire. We’re happy to help.

Terra’s David Martin Debuts his New Real Estate Column in Forbes

David Martin

A warrior and a poet? Meh. Maybe not, but David Martin, head of Terra Group and developer of Grove at Grand Bay, Park Grove, and GLASS, is now a developer and an author. He’s writing a twice-monthly column over at Forbes on ‘real estate development, design, and sustainability,’ beginning with a discussion on why more buyers in South Florida are end users these days as opposed to speculators. To summarize his point in just a few words: Miami’s a bit more grown up, and that makes a big difference.

Week in Review: How to Avoid the Federal Disclosure Law for Cash Purchases and Other News…

Rendering from Paramount Miami Worldcenter

Week of January 17-23, 2016.

The US Treasury announced this week that starting in March, title companies will be required to disclose the identities of buyers to government regulators for all cash purchases above $1 million in Miami’s residential real estate market. They are hoping to put a stop to illicit funds being laundered through the cash purchases, but effectively are also spooking legitimate buyers who simply do not wish to have their buying habits publicly disclosed.

Fear not, fancy condo shoppers. The ink is not even dry on the new order and The Real Deal has already compiled a list of 7 ways that the rule can be circumvented. [The Real Deal]

Last week, the developer of Miami Worldcenter announced that it is scrapping the plans for an enclosed mall just days after Macy’s announced multiple store closings due to slow sales. After this announcement Taubman and Forbes cancelled their contract with Worldcenter, causing a flurry of rumors and news stories stating that the project would be scrapped. It turns out that everyone jumped the gun. According to the developer and this Taubman release, the project is not scrapped. The contract just needs to be renegotiated to reflect the new building plans. [Zacks]

While everyone was up in arms about the potential drama at Miami Worldcenter, Brickell CityCentre released their updated list of all retailers, shops and restaurants that will be opening with the mall. The shops will begin individual build-out soon and is scheduled to open later in the year. [The Next Miami]

In possibly the least surprising news of the week, Car2Go finally announced that they are suspending service effective March 1. They say that the reason for the service-shuttering is low ridership and high state taxes, locals have not wasted time or minced words with their own theories. It seems they have been in trouble with their client base for some time due to poor handling of a PR incident involving a drunk driving accident, not offering service in many important areas of the community, poor customer service and unreliable service. We think it can be easily explained by simple economics… why pay more to drive yourself in a shared smart car with a complicated service when you can pay less and have an Uber car pick you up at your doorstep and drop you off wherever you want to go? The choice is simple. [Curbed]

DEAL ALERT: Developers Offering Attractive Close-Out Pricing on Existing Condos

While the market is buzzing with attractive pre-construction investment deals, not many people think to inquire about the buildings that are existing and still have a bit of inventory. For some investors, these existing buildings can bring a better investment than the speculative development deals that others are flocking to. The close-out phase of an existing building is actually one of my favorite times to sell in a project for a few reasons:

- Mitigated Risk

The investor can see the actual building and apartment they are buying, so much of the risk of the design and construction phase has gone by. Since the apartment exists already, the buyer knows exactly what they will receive, not a photo of a building that they hope comes to fruition the way it is shown in the rendering.

- Faster Return

If you buy existing inventory for purposes of a rental investment, you can lease the property immediately. You will be able to see your money work for you straight away while other investors wait to see how their investments will perform after the building is completed.

- Financing

Mortgages become far easier after half of the apartments in a development have closed. Since the lender can also see the building, they know what their risk is and are more willing to lend money with lower down payments. This is true for both local and international investors.

- Flexibility

Developers are investors too, and when they are in the close-out phase they are almost finished with their project. I don’t care how many people say that there is no emotion in business, that is wrong. There is something emotional about being close to the finish line and that makes developers more eager to sell those last apartments to get to their goal. Many times we see developers offering HOA credits, discounted prices and special leaseback programs to entice buyers into helping them reach their goal. If buyers can reach their goals by helping developer reach their goals, isn’t that a perfect scenario? I think so…

With these points in mind, I have a prime example of a building that is currently in this situation.

City24 is a boutique luxury building in Edgewater with 119 apartments. It was originally built in 2008 and has all of the amenities and finishes that residents of the neighborhood have come to expect. There is a 24 hour doorman, gym, pool & jacuzzi, secured garage parking, the apartments have stainless appliances and quartz countertops with tile or wood floors, washer/dryers in the apartment, pretty views, easy accessibility to restaurants and fun events… the things we look for in the Downtown Miami area.

Out of the 119 original apartments, the developer needs to sell only 6 more in order to be finished. We have toured the remaining 6 and have not seen a reason that these specific apartments remain unsold. The developer is offering the full inventory for $2.5M, which works out to roughly $385/square foot. Naturally, if one investor were to purchase all 6 apartments, a lower price or additional perks would be considered.

At the offered price, the remaining apartments would equate to a pre-tax return of 5% when rented for full market value. The typical investment apartment in the area today brings a 3% return, so the buying investor would start off with an advantage on this package. Additional parking spaces, HOA credits or price negotiations would help the both the buyer and the seller while making good use of the property.

If you would like more information on specific apartment numbers, sizes, prices or packages, don’t hesitate to reach out. We can work together to present a package that meets your investment goals on this or similar projects.

Developers Offering Year-End Incentives to Close Out Projects

In an effort to hold the attention of buyers and sell as many apartments as possible before the end of 2015, developers are coming out with attractive incentives packages to help buyers decide to act now and close out their projects. Here are some of our favorite incentives from buildings that are currently under construction and selling pre-construction residences:

Brickell Heights – Related has lowered the down payment requirement to 30% from the original 50%. Prices of remaining inventory start in the $400,000’s.

SLS Lux – All of the condo/hotel apartments are currently under contract, but the developer is offering upgraded kitchens on the remaining condo residences and 30% down payment. The penthouse collection has recently been released and sales are almost finished. Prices start in the $600,000’s for the remaining units.

Paraiso Bayviews – All four towers of the Paraiso development are currently under construction and Paraiso Bayviews is 95% sold. For select apartments, the developer is offering a finishes package with porcelain flooring throughout. The prices currently start in the mid $500,000’s up to the high $600,000’s and penthouses are priced between $639,900 to $1.75MM. The developer has not officially offered deposit flexibility but has indicated that it is possible on a case-by-case basis.

Hyde Midtown – The construction of Hyde Midtown has only just started in recent months, but close out is fast approaching. Prices on remaining inventory start in the $400,000’s and the sales team has offered some flexibility on the 30% down payment on a case by case basis.

We were very happy to see these flexible down payment options, as it will make new condo purchases more accessible to those who hope to live in the apartments. The incentives also help to allow for the possibility of financing the condo purchases, which many people have inquired about yet been unable to easily attain until now.

Let us know if you or someone you know is interested in more information on these or other developments. We will have team members in Miami during all of the holidays and until the end of the year to help visitors by appointment.

The Crimson in Edgewater Gains Fannie Mae Approval; Prepares to Start Closings

Placed between IconBay and Bay House in Miami’s Edgewater neighborhood, The Crimson is preparing to begin closings this month. The Crimson is a boutique property of only 90 apartments in 20 floors and will offer a more private lifestyle than some of the larger projects on either side.

One of the aspects of The Crimson that we love is its status of being silver LEED certified – meaning that the project has earned 50-59 points toward ultimate energy efficiency. Builders can earn LEED certification points through building design, quality of materials, efficiency of appliances and even for designing low-maintenance projects.

To prepare for the opening, the developer has also announced that the project is Fannie Mae approved. This is particularly exciting for local residents who are interested in purchasing an apartment as their primary residence. The sad reality is that many projects in the area are not attainable for local buyers due to the fact that mortgage funds are not typically available to buyers of new projects. Buyers can now purchase a brand-new condo in The Crimson with as little as 20% down payment. There are only 5 buildings in the greater Downtown area that have this Fannie Mae approval.

There are still a few opportunities to purchase prior to the building opening with prices ranging from $455,000 up to $1,579,000.